Brazil — one of Latin America’s largest and most dynamic economies — attracts entrepreneurs from all over the world. This guide explains how foreigners can open and run a company in Brazil, covering every step from legal requirements and taxation to real-world case studies of successful foreign founders.

Opening a Business in Brazil: Comprehensive Guide for Foreign Entrepreneurs (2025)

Starting a business in Brazil Brazil – the economic powerhouse of Latin America – offers immense opportunities for entrepreneurs with its market of over 210 million consumers. Foreign investors are allowed 100% ownership of businesses in Brazil, making it an attractive destination for global entrepreneurs, including those from Russia and other countries. However, turning this opportunity into a successful enterprise means navigating Brazil’s complex bureaucracy, legal requirements, and tax system. This guide provides a step-by-step encyclopedia-level roadmap to as a foreigner, covering everything from choosing a company structure and registering for a CNPJ to obtaining visas, permits, understanding taxation, and even real-world case studies.

Whether you’re planning to open a café in Florianópolis or launch a tech startup in São Paulo, this guide will walk you through every stage – incorporating best practices and up-to-date (2025) information to ensure your venture is set up for success.

Can Foreigners Open a Business in Brazil?

{kind=link}

Yes. Brazil permits foreign individuals and companies to open and own businesses with no requirement to have a Brazilian partner. In most sectors, foreigners can even own 100% of the equity. But there are important legal requirements and a few industry restrictions to be aware of:

-

Local Legal Representative: If a foreign owner does not reside in Brazil, you must appoint a Brazilian resident as an official legal representative (proxy) with power of attorney. This representative will act on your behalf for tax, legal, and regulatory matters. Typically, the representative can be a trusted lawyer or accountant in Brazil. (If you do reside in Brazil, you can fulfill this role yourself as a managing partner, but you’ll need the appropriate visa/status – see Visa section below.)

-

Brazilian CPF Number: All foreign shareholders (individuals) and any foreign directors must obtain a CPF (Cadastro de Pessoa Física), which is the Brazilian individual taxpayer identification number. The CPF is required to be listed in the company’s incorporation documents, essentially to identify foreign investors to Brazilian authorities. A CPF can be obtained from a Brazilian consulate abroad or directly from the Federal Revenue (Receita Federal) in Brazil, even if you don’t live in Brazil.

-

Registered Business Address: Your company must have a registered address in Brazil (a physical location for the business headquarters). This can be an office, commercial space, or even a virtual office address, as long as it is a valid address where the company will be domiciled for legal purposes. Different business activities have zoning requirements, so ensure the address is allowed for the intended business (for example, some home addresses may not be allowed for commercial activities requiring an operating license).

-

Apostilles and Translations: If you have corporate documents from abroad (e.g. a parent company’s documents, or power of attorney papers), they must be apostilled in your home country and translated by a sworn translator (tradução juramentada) into Portuguese. These legalized documents will be needed during the company registration process. Similarly, passports and proof of address might need to be officially translated for certain filings.

-

Sectors with Restrictions: The vast majority of industries are open to foreign-owned companies. However, a few sectors have restrictions or special rules for foreign capital. For example, journalism and broadcasting businesses have limits on foreign ownership; private security companies must have 100% national (Brazilian) capital; acquisition of rural properties in border areas by foreign-owned companies requires special government authorization; and certain types of transportation (especially related to aerospace or highway freight) may have restrictions. Always check if your intended industry has any foreign ownership caps or licensing hurdles. (Fortunately, in “the vast majority of cases” there is no impediment – foreign investors can operate freely.)

-

Investor Visainvestor visa Visa Considerations: You do not need a Brazilian visa or residency just to open a company. In fact, the entire incorporation process can be done remotely by granting power of attorney to your Brazilian representative. Many foreigners open businesses in Brazil without ever setting foot in the country – an appointed local lawyer can handle filings on your behalf. However, if you plan to live in Brazil and actively manage the business, you will need an appropriate visa or residency permit. The common pathway is an (Permanent Residency), which typically requires a minimum investment of R$500,000 (approx. USD $100k) in your Brazilian business. In recent years, Brazil introduced a startup visa option requiring a lower investment (~R$150,000) if invested in an approved innovative startup venture. If you obtain an , you’ll receive a CRNM (National Migration Registration Card), formerly known as RNE, which proves your legal residency. (For those who only want to run the business remotely or through local managers, no visa is required – you can remain abroad and still be the owner.)

-

Documents for Foreigners: In summary, a foreign entrepreneur should have: passport copies, proof of overseas address, Brazilian CPF number, and if not residing in Brazil, the ID/CPF of the Brazilian representative. All foreign documents must be apostilled and translated as needed. These will be used in the preparation of the company’s Articles of Association and for various registrations.

Real-World Note: Opening a company in Brazil involves many bureaucratic steps, and local expertise is crucial. As one Russian entrepreneur cautioned, “Starting a company in Brazil is a process with many nuances. Before relying on local specialists, you should at least minimally understand the basics of legislation, tax law, and accounting, otherwise you risk receiving low-quality services.” In other words, educate yourself (as you’re doing now!) and choose trustworthy advisors – it will pay off in avoiding delays and mistakes.

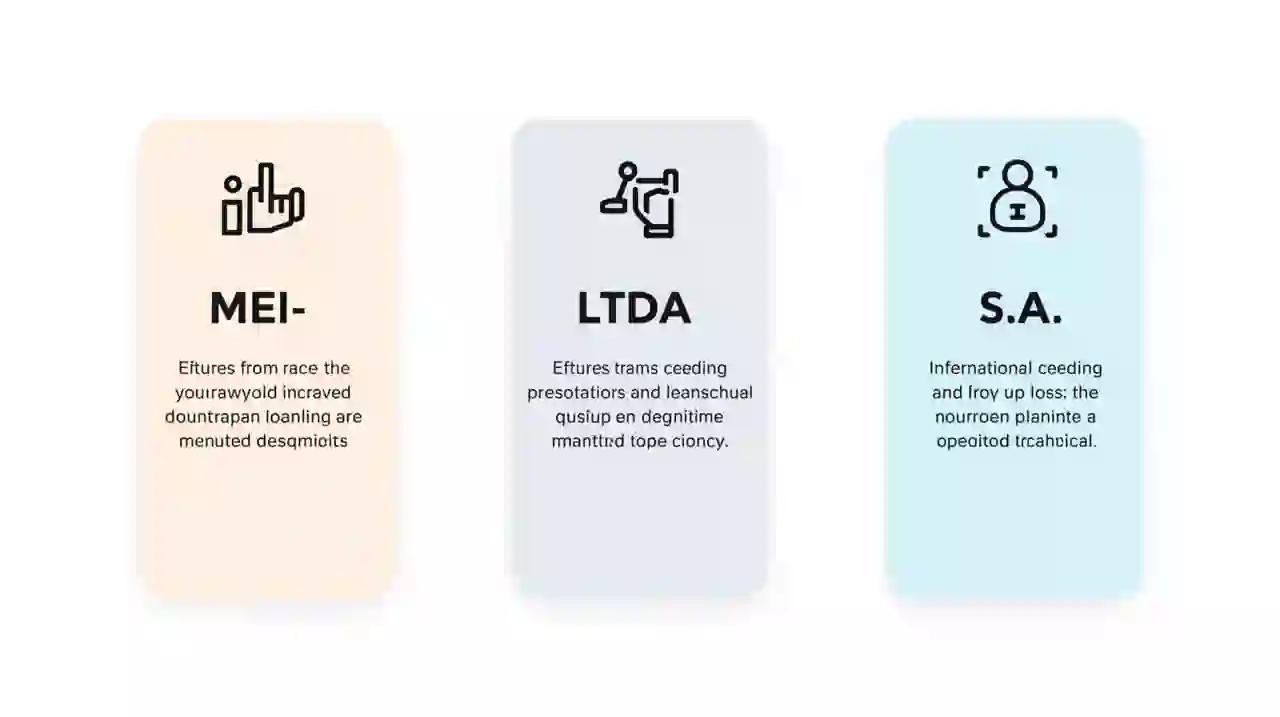

Choosing the Right Business Structure in Brazil

{kind=link}

One of the first decisions is selecting the legal structure for your new company. Brazil offers several types of business entities, but foreign entrepreneurs typically choose among a few key options. The choice will affect your liability, tax obligations, ability to have partners, and regulatory complexity. Below are the most common structures:

-

MEI (Microempreendedor Individual) – Individual Micro-Entrepreneur. This is a simplified form of sole proprietorship for very small businesses. It allows a single person to register as a company (with a CNPJ) under greatly simplified tax and reporting rules. MEI is capped at low revenue (currently R$81,000 per year, about US$16k) and you cannot have business partners or investors – it’s just you as the owner-operator. The upside is a MEI pays only a fixed monthly tax (around R$60) covering all taxes and social security, and has minimal bureaucracy. Foreigners can register as MEI if they are legal residents in Brazil with an RNM (foreigner ID card) – “Yes! If you are an immigrant you can also be MEI. You only need your CRNM (RNE/RNM) number…”. For a newly arrived foreigner not yet holding residency, MEI won’t be available; in that case, you’d choose another structure below. MEI is ideal for freelancers, solo consultants, and small traders starting out, including many digital entrepreneurs (e.g. an online tutor or a craft seller could start as MEI). Keep in mind MEIs cannot have employees (except one assistant) and if you exceed the revenue limit, you must transition to a higher category.

-

LTDA (Sociedade Limitada) – Limited Liability Company (LLC). This is by far the most common business structure in Brazil for companies of all sizes, including those with foreign owners. An LTDA is a private company that can have one or more owners (quotaholders) and provides limited liability – your personal assets are protected, and liability is limited to the capital invested. Historically, an LTDA required at least two partners, but since 2019 it’s possible to form a single-member LTDA (called Sociedade Limitada Unipessoal, SLU) without needing a second shareholder – effectively replacing the old EIRELI form (see note below). There is no minimum capital requirement for an LTDA by law (aside from certain industries) – you can start with even R$1, though in practice you should invest enough to cover startup costs and show credibility. Foreigners can own 100% of an LTDA, and it’s the simplest vehicle for foreign investment. An LTDA must have a Contrato Social (Articles of Association) and comply with corporate formalities, but it’s less complex than a corporation (S.A.). Most foreign-owned businesses in Brazil are LTDA companies because of their flexibility – whether it’s a small consulting firm or a medium-sized trading company. One thing to note: a standard LTDA requires at least one administrator (manager) who must be a Brazilian resident (either a citizen or foreigner with residency). This ties back to the requirement of a local representative – typically the administrador of the LTDA will be your Brazilian representative if you, as a foreign owner, live abroad.

-

EIRELI (Empresa Individual de Responsabilidade Ltda.) – Individual Limited Liability Enterprise. This form was essentially a one-person company with limited liability, requiring a high minimum capital (at least 100 times the Brazilian minimum wage). Important: As of 2021, Brazil eliminated new EIRELI formations – the single-person LTDA (SLU) now serves the same function without a capital requirement. Existing EIRELIs were converted to LTDA entities. For practical purposes, foreign entrepreneurs no longer need to use EIRELI; you would form an LTDA even if you’re the sole owner. We mention it only because older resources reference EIRELI for sole proprietors – but now a solo foreign investor can do an LTDA/SLU with no Brazilian partner needed and no special capital, greatly simplifying things.

-

A. (Sociedade Anônima) – Corporation or Joint-Stock Company. An S.A. is a more complex legal entity akin to a C-corporation. It can be privately held or publicly traded. S.A.’s are governed by a specific corporate law, require a board of directors and an executive team, must publish financial statements, and have more rigorous reporting. They allow raising capital through shares, and are the structure required if you plan an IPO or to issue certain securities. Foreigners can own S.A. shares, but an S.A. must have at least 2 shareholders at all times (no single-shareholder S.A.). Typically, small entrepreneurs do not choose S.A. due to cost and complexity; it’s used by larger businesses or those needing equity investors. If you have a startup that will seek venture capital, you might consider migrating from LTDA to S.A. down the road. Initially, most start as LTDA and later “upgrade” if necessary. For completeness: an S.A. also has a minimum capital requirement if it’s publicly traded (and certain industries like banking require S.A.), but an ordinary closed S.A. can theoretically start with modest capital. The tax regime for S.A. is usually Lucro Real (actual profit, see Tax section) by default, as they can’t use Simples Nacional or other simplified regimes.

-

Other Forms: Brazil also recognizes Sole Proprietorship (Empresário Individual) – basically a personal business without limited liability (not advisable for most, since you’d be personally liable for debts). There are also business cooperatives, partnerships, etc., but these are niche. In almost all cases, a foreign entrepreneur will choose either an LTDA (with either one or multiple partners) or operate as an MEI if qualifying as a resident individual with a very small business. If you scale up significantly, you might then incorporate as an S.A.

Below is a quick comparison of key features of common business forms:

| Feature | MEI (Micro Entrepreneur) | LTDA (Limited Company) | S.A. (Corporation) |

|---|---|---|---|

| Allowed Owners | 1 individual only (must be Brazilian or legal resident) | 1 or more individuals or companies (foreign or local) | Minimum 2 shareholders (can be individuals or entities) |

| Liability | Unlimited personal liability (no separation of assets) | Limited liability (owners’ liability = their quota capital) | Limited liability (shareholders not personally liable) |

| Minimum Capital | None (no stated minimum; very low startup cost) | No legal minimum (a token capital is allowed, though adequate funding is recommended) | No fixed minimum by law for private S.A., but substantial capital needed for certain purposes (e.g. R$100k for public registration) |

| Tax Regime Eligibility | Simples Nacional only (default) – simplified micro-business tax | Can opt for: Simples Nacional (if qualifying as small and no forbidden shareholders), or Presumed Profit, or Actual Profit regimes | Cannot use Simples. Generally uses Presumed or Actual Profit (large S.A.s must use Actual Profit) |

| Complexity & Compliance | Very low: Online registration, no formal accounting needed (simple ledger), simplified annual reporting. | Moderate: Requires formal Articles of Association, registration at commercial board, an accountant for books and taxes, annual financial statements (though simpler than S.A.). | High: Requires Board of Trade registration and registration with CVM if public, a board and officers, published financials, independent audits (if public), shareholder meetings, etc. |

| Ideal For | Solo entrepreneurs (freelancers, artisans, small traders) operating on a very small scale (≤ R$81k/year). | Small to medium businesses, typical startups, any foreign investor-owned company. Most common choice for everything from consultancies to restaurants to import/export firms. | Large businesses, companies planning to raise significant investment or go public, or required sectors (e.g. banks, insurance). |

Note: If you plan to remain a very small enterprise, MEI offers extreme simplicity. But if you expect to grow or have partners/investors (or if you aren’t yet a resident), an LTDA is usually the way to go. Many foreign entrepreneurs start an LTDA even as a single-person venture due to its flexibility.

Also, be aware that Simples Nacional (simplified tax) regime (discussed later) is available only to certain types of companies. Notably, a company that has another company as a shareholder cannot opt for Simples. This means if your Brazilian company is owned by another foreign company (instead of directly by you as an individual), it might be barred from Simples. Most individual foreign entrepreneurs hold shares personally, which is fine – you can still use Simples if you meet the size criteria. The restriction is mainly if, say, “XYZ Corp (USA)” opens a subsidiary in Brazil – that Brazilian company cannot use Simples due to having a corporate shareholder. In such cases, the company must use the standard tax regimes (Presumed or Actual Profit). We’ll dive into these regimes in the Taxation section.

Step-by-Step Guide: How to Open a Business in Brazil (Foreigner’s Roadmap)

{kind=link}

Opening a business in Brazil involves several sequential steps, dealing with different government agencies at the federal, state, and municipal levels. Below is a comprehensive step-by-step guide, from planning to post-registration, incorporating the requirements we’ve discussed:

Step 1: Plan Your Business and Choose a Legal Structure

Before plunging into paperwork, clarify your business plan: What product or service will you offer? Will you need a physical location or is it online? How large do you expect it to grow? A solid plan will inform your choices in the next steps.

Choose the appropriate business structure (MEI vs. LTDA vs. S.A., etc.) as discussed in the previous section, based on your ownership and growth plans. For most foreign entrepreneurs, the choice will be Sociedade Limitada (LTDA) for its liability protection and flexibility. If you qualify and your business is tiny, consider MEI for simplicity. If you’re setting up a major venture or seeking investors, you might start planning for an S.A. but it’s usually not the initial form.

Also, pick out a business name (or a few alternatives). Brazil requires that company names be unique within the state and usually include a description of the business activity. As part of the registration, you’ll conduct a name availability search with the State Commercial Registry (Junta Comercial). For now, have an idea of your desired name and a backup or two. The name typically must have a designator (e.g., “Ltda.” at the end for an LTDA).

Step 2: Obtain a Brazilian CPF (Tax ID) for All Founders

{kind=link}

As noted, a CPF number is mandatory for any foreign individual who will be a partner (shareholder) or director of the company. If you don’t already have one, this is a first critical step. You can apply for a CPF from abroad at your nearest Brazilian Consulate/Embassy, or in Brazil at a Banco do Brasil, Caixa Econômica, or Correios branch, or online through the Receita Federal’s system (for some nationalities). The process involves filling a form and providing identification; if done abroad, the Consulate will forward the request. CPF issuance is usually quick (same day) and costs very little or is free.

Make sure each foreign shareholder (and any foreign person who will be listed as a director/manager) has their own CPF. If any shareholder is a foreign company rather than an individual, that company will need to obtain a CNPJ (corporate tax ID) in Brazil as a foreign entity, which is a bit more complex – often handled later in tandem with incorporation. (Most often, foreign entrepreneurs use personal names/CPF to register, unless it’s a large international firm expanding into Brazil.)

Step 3: Appoint a Legal Representative (Proxy) in Brazil

{kind=link}

If you (the owner) will not be residing in Brazil, you must appoint a legal representative who is a resident of Brazil. This person will be your proxy (procurador) for managing the company’s legal affairs with the government. Commonly, people hire their law firm or accountant to fulfill this role, but it could also be a trustworthy colleague or family member in Brazil.

The representative will need to sign a Power of Attorney (Procuração) prepared by your lawyer, which authorizes them to act for you in incorporation and tax matters. Your signature on this document (if signed abroad) must be notarized and apostilled, and then translated to Portuguese. The power of attorney typically states specific powers, like signing the incorporation papers, representing before Receita Federal and Central Bank, etc..

If you are planning to move to Brazil immediately and have a residence visa in process, you might be able to be present and sign as the administrator. But even so, having a local proxy is highly useful for the incorporation process and bureaucratic follow-up.

Tip: Choose someone reliable and experienced. They will essentially be the face of your company to authorities until you can take over. Many foreign entrepreneurs engage a lawyer to be the formal representative and an accountant to handle tax registrations – some firms specialize in providing this “representation” service. For instance, Martin Law states, “Our attorneys can serve as your official legal representative in Brazil, handle all document requirements, and guide you through every stage of incorporation” – such services can ease the process but come with fees. If you go without a lawyer, ensure your proxy understands Brazilian bureaucracy.

Step 4: Draft the Articles of Association (Contrato Social)

Now the actual company formation begins. You (and your partners, if any), with help of a lawyer or accountant, will draft the Articles of Association (in Portuguese: Contrato Social for LTDA, or Estatuto for S.A.). This is the founding document of the company, equivalent to a partnership agreement or bylaws. It will include key details such as:

Company Name and purpose.

Business Address (headquarters).

-

Partners (Quota Holders) names, nationalities, CPF/CNPJ numbers, and their share in the capital.

-

Share Capital (Capital Social) – how much money (or assets) is being invested into the company, and the division of quotas (shares) among partners. (There’s no minimum for LTDA, but the amount should realistically cover initial operations. You could start with a low amount and increase later if needed. Importantly, if you are pursuing an Investor Visa, note that the visa requires a certain capital injection – e.g. R$500k or R$150k – which should be reflected in the capital and actually invested in a Brazilian bank account.)

-

Company Administration – who will act as the administrator or manager (the person with authority to represent the company legally). Typically one of the partners (or an outsider) is named as the Administrador. If a foreigner will be the administrator, they must have Brazilian residence. If none of the foreign owners reside in Brazil, usually the legal representative (proxy) is named as an interim administrator. You can later change the administrator via an amendment when you (the owner) get your visa or appoint someone else.

-

Business Activities – a description of what the company will do, often referencing CNAE codes (the official classification of economic activities).

-

Any special clauses like how profits will be distributed, how decisions are made, arbitration clause, etc.

For an LTDA, the Contrato Social must be signed by all partners (or their legal proxies via PoA). If signed abroad by you, it will need to be notarized, apostilled, and translated, or you can sign it in Brazil with your proxy under the power of attorney.

This step typically requires a Brazilian lawyer or experienced accountant to prepare correctly. They will ensure it meets all legal requirements under the Brazilian Civil Code and local Board of Trade regulations. Accuracy is important – errors in the contract can cause rejection or future problems. For example, Ksenia (the café owner from Russia) mentioned that her first accountant made mistakes in the legal registrations, causing numerous headaches later. Don’t let that happen – get the contract right from the start.

Foreign Investment Registration: If any partner is a non-resident (which in this case they are), after the company is formed, you will need to register the foreign capital with the Central Bank of Brazil (we will cover this in Step 8, but keep in mind it’s related to the capital you declare in the Contrato Social). Essentially, Brazil tracks foreign direct investment through an online system (RDE-IED), which you must update whenever you bring money in or out. The initial capital must be reported, but this reporting is done after you have the company’s CNPJ and bank account, not at the moment of drafting the contract. Just be aware that whatever amount you declare as capital, you should plan to actually remit to Brazil so it can be registered as FDI (this is what proves to the government that you invested and allows future profit repatriation).

Step 5: Register the Company with the Board of Trade (Junta Comercial)

{kind=link}

Once your constitutive act (Contrato Social or equivalent) is ready, the next step is to register your company with the State’s Commercial Registry. Each state in Brazil has a Junta Comercial that approves and archives company incorporation documents.

Name Search: Before formal submission, a name availability check is done. Your advisor can usually do this online. Reserve the name if possible. Then, prepare the required documentation for filing which generally includes: - The signed Contrato Social (or incorporation act), with translations if needed. - Copies of partners’ documents (passports, CPF, proof of address, for individuals; or corporate docs for any corporate partners, duly apostilled and translated). - Proof of payment of registration fees (Junta Comercial has a filing fee, which might be on the order of a few hundred reais depending on the state). - Application forms provided by the Junta (some states have an online portal where data is input and forms generated).

Submit these to the Junta Comercial of the state where your company will be headquartered. Many states (like São Paulo, Rio, Santa Catarina, etc.) now have online or integrated registration systems, meaning you might submit electronically through a system called REDESIM or the Junta’s website. In other states, you might need to submit physical documents.

Processing time: Historically, this could take several weeks (and Wise’s guide still notes 60–90 days for the overall registration process). However, there have been improvements. Some states have dramatically sped up approvals – “States like São Paulo, Santa Catarina, and the Federal District now process business registrations in one day” thanks to digital transformation. In the best case, your company’s constitutive act could be approved within 1–5 business days. Let’s assume a couple of weeks for safety, as delays happen if any document is missing or if there’s a high volume of filings.

When the Junta Comercial approves, they will officially register your company and issue a document (proof of registration and a company registration number at the Junta).

CNPJ Simultaneous : Brazil has an integrated system such that upon Junta approval, the data is forwarded to the federal tax authority (Receita Federal) to issue your CNPJ (the National Registry of Legal Entities number). In many cases, you don’t need a separate application for CNPJ – it comes automatically after the Junta registration is confirmed. The CNPJ is analogous to a company’s tax ID or EIN. It’s a 14-digit number formatted like XX.XXX.XXX/0001-YY.

Step 6: Obtain Your CNPJ and Register for Federal Taxes

{kind=link}

CNPJ After Junta Comercial registration, you should receive your from the Receita Federal (often this is an online certificate you can download from the Receita’s website using the company name or Junta registration number). The CNPJ registration is what allows your company to exist as a legal entity for tax purposes – “This number allows you to operate legally, issue invoices and hire employees.”. Think of the CNPJ as the corporate identity number you’ll quote on all invoices, contracts, and tax filings.

At this stage, your company is officially formed – congratulations! 🎉 But it’s not ready to do business until you complete the next steps of tax and license registrations.

CNPJ Enroll Foreign Shareholders in CPF/: One sub-step often done at this point (if not already completed) is making sure any foreign shareholder that is a legal entity has been enrolled in the National Registry of Foreign Corporate Taxpayers (CNPJ for foreign company) and any individual shareholders have their CPF linked. In practice, because you provided CPF for individuals and all needed data, this is usually taken care of. If a foreign company was a partner, additional filings with Receita Federal (through a specific form called DBE) might have been necessary. Your legal representative typically handles this. Essentially, by the time you have the CNPJ, Receita Federal knows the foreign ownership and may require that the foreign investor has appointed a Brazilian tax representative as well (often the same person as the legal rep).

Digital Certificate: It is highly recommended (and sometimes effectively required) to obtain an e-CNPJ (digital certificate) for your company at this point. This is a secure digital ID (on a token or in the cloud) used to sign documents, issue Nota Fiscal eletrônica (invoices), access government systems, etc. To get one, the legal representative or administrator will go (in person) to an authorized Certification Authority office with documents. This enables online tax compliance. Many accounting firms will do this for you as part of their setup.

Step 7: Register with State and Municipal Authorities; Obtain Licenses

{kind=link}

With a CNPJ in hand, you must register your company with applicable state and city authorities and obtain necessary operating licenses. This part ensures your business is fully compliant to actually start operations:

-

CNPJICMS State Registration (Inscrição Estadual): If your company will engage in commerce (buying/selling goods), manufacturing, or other activities subject to state tax (), you need to register with the State Department of Finance for an Inscrição Estadual (IE). This is essentially a state tax ID. For example, if you open a retail shop or import/export business, ICMS (VAT on goods) applies and you must have IE to issue the required invoices. Service-only companies (which pay ISS, a city tax) often do not need state IE unless they also sell products. Some states automatically issue the IE together with the via the integrated system. In others, your accountant must apply to the state’s SEFAZ (finance secretariat) for the inscription.

-

CNPJ Municipal Registration (Inscrição Municipal): Similarly, if your company provides services, you must register with the Municipal Tax Authority (city hall) to obtain an Inscrição Municipal (IM). This registration allows you to pay the ISS (Service Tax) and also is required to obtain your alvará (business license). Typically, once you have , you go to the city’s online system or department (many large cities have online integration too) and apply for the municipal registration. In some places, this is part of the integrated REDESIM process. The IM number is used on service invoices (Nota Fiscal de Serviços).

-

Operational License (Alvará de Funcionamento): This is the formal business license from the city authorizing you to operate at a given location. You’ll apply through the city government, often at the same time as the municipal registration. You have to inform the business address and the specific activity; the city will verify zoning laws to ensure your address can host that type of business (for example, a factory can’t be in a residential zone, a food business must meet health codes, etc.). Sometimes fire department approval and building inspections are required before the license is granted. Many cities issue a provisional license quickly if the activity is low-risk, then follow up with inspections. Ensure you meet any requirements (e.g. installing fire extinguishers, accessibility features if you have a physical shop open to public, etc.).

-

Additional Permits: Depending on your industry, you may need special permits:

-

Health and Sanitary Permit (Vigilância Sanitária): Required if you deal with food, beverages, restaurants, medical services, cosmetics manufacturing, etc. Basically anything impacting public health. This usually involves an inspection by the health surveillance agency (often referred to as VISA or Anvisa if federal-level).

-

Fire Department License (Habite-se or AVCB): If your business operates in a commercial space, the fire department may need to inspect and issue a safety certificate (AVCB in some states). For a small office, this might be covered by the building’s certificate. For a restaurant or shop, you definitely need one.

-

Environmental License: If your business could impact the environment ( factories, certain chemicals, even some software companies if they use large generators, etc.), environmental agency approvals might be needed.

-

Professional licenses: Some activities (like engineering, law, medicine) require the business and/or professionals to register with a professional council (e.g., CREA for engineering firms, OAB for law firms).

Make sure to research the specific licenses for your line of business. For most ordinary businesses (like opening a consulting firm, a café, a retail store), the key ones are the municipal operating license and maybe a fire inspection. If you’re doing something specialized (food production, education, transportation), check the sector regulators.

Completing the state and municipal registrations essentially “activates” your company for operation in all jurisdictions. At this point, you have all the tax IDs required to collect and pay taxes on your activities.

ICMS Nota Fiscal: Once registered with tax authorities, your company will need to activate its electronic invoicing capability. Brazil requires businesses to issue Nota Fiscal (NF) for sales of goods and services – these are official electronic invoices that get reported to the government. There are different systems: NF-e (model 55) for goods ( invoices) and NFS-e for services (ISS invoices) by municipalities. You should: - Register for access to the NF-e system (usually done automatically when you get IE and have a digital certificate). - For services, register with the city’s Nota Fiscal service online platform.

Each invoice series will use your CNPJ, and you’ll need your digital certificate to sign them. It’s critical to have this in place before you make your first sale, because failing to issue required notas can result in fines.

As Martin Law emphasizes in their checklist, “Activate electronic invoicing (Nota Fiscal) by registering your company with the tax authorities’ digital system.” This is often one of the final steps to be fully operational.

Step 8: Register Foreign Investment with the Central Bank (RDE-IED)

This step is unique to foreign-owned companies. Whenever foreign capital enters Brazil as an investment in a company, the law requires it to be registered in the Central Bank’s Electronic Declaratory Registry for Foreign Direct Investment (RDE-IED). This is done online (often by your accounting or law firm) through the Central Bank’s system (called Sisbacen).

Right after your company is set up and you have a Brazilian bank account (next step), you’ll likely transfer the initial capital (the money you pledged as capital in the Contrato Social) into the company’s Brazilian bank account. Within 30 days of the funds arriving, you must report that inflow via the RDE-IED system. You’ll log the amount, the date, the currency, the investor’s details, and tie it to your company’s registration.

This registration serves a few purposes: - It legitimizes the investment as FDI, proving that money came from abroad lawfully. - It is required to repatriate capital or remit dividends later on. If you want to send profits back to your home country, the bank will ask for proof that the capital was registered, and that yearly economic-financial statements have been filed in the Central Bank’s system (there is an annual declaration for foreign-owned companies if assets or capital are above a certain threshold). - It keeps Brazil’s statistics on foreign investment up-to-date (legal requirement).

Your legal representative or a specialized consultant can handle the RDE-IED registration. It’s not a public process like Junta Comercial – it’s an internal Central Bank filing. After the initial capital registration, you also must update the system for any future changes: e.g. new capital contributions, reinvestment of profits, distribution of dividends to foreigners, changes in ownership percentages, etc. It’s wise to have an accountant manage this to stay in compliance.

Skipping this step is dangerous – unregistered foreign investment can lead to difficulties and fines, especially if you try to send money out. So don’t overlook it. It’s a relatively quick online procedure if you have all data.

Step 9: Select Your Tax Regime and Set Up Accounting

Brazil’s tax system is multi-layered and you have to choose a tax regime for your company that will determine how you calculate and pay taxes. Upon registration, typically your company is by default in the Lucro Presumido (Presumed Profit) regime unless you opt into Simples Nacional or are required to use Lucro Real (Actual Profit). Here’s a quick overview to make that choice:

-

CNPJSimples Nacional: A simplified regime for small businesses (annual gross revenue up to R$4.8 million). It consolidates federal, state, and municipal taxes into one monthly payment. The tax rate is a percentage of gross revenue, varying by industry and revenue level – starting around 4% to 6% for most small services or commerce, and gradatively increasing in brackets. Simples greatly reduces paperwork: you pay a single DAS tax boleto and don’t have to file separate federal tax returns for each tax. Most new small businesses prefer Simples if eligible, because of lower tax burdens and simpler compliance. Foreign-owned companies can opt for Simples if and only if they do not fall under exclusion criteria (as mentioned, having a foreign company as a shareholder is an exclusion; having a partner that is also an owner of a large company can be an exclusion; being in certain sectors like finance, or being a branch of a foreign company, are excluded). But a typical foreign individual setting up a startup can use Simples – there is no rule forbidding foreign individual shareholders in Simples. For example, if you open a small restaurant or an IT consulting LTDA, you can likely elect Simples Nacional. You usually make this election in January. New companies have a window (within 30 days of issuance or by a certain date) to apply for Simples in the current year. If you miss it, you operate under Presumed Profit for the year and then switch to Simples the next January.

-

Lucro Presumido (Presumed Profit): This is a simplified regular regime for medium businesses or those not eligible for Simples. Under Presumed Profit, you pay corporate income taxes (IRPJ and CSLL) on a deemed profit percentage of your revenue, rather than actual profit. For example, a service business might have a presumed profit margin of 32% – meaning you pay income taxes on 32% of your gross revenue, regardless of your actual profit. The effective income tax rate would be 15% of that presumed profit for IRPJ plus 9% CSLL, which works out to about 7.68% of gross revenue for IRPJ+CSLL (plus there are PIS/COFINS taxes of ~3.65% on gross, etc.). If your actual profit is much higher than the presumed margin, Presumed Profit is beneficial (because you’re taxed only on the lower presumed amount). If your actual profit is lower, you still pay on the higher presumed amount – so it can hurt low-margin businesses. This regime requires quarterly calculations and paying of taxes, but simpler bookkeeping than Lucro Real. Companies up to ~R$78 million annual revenue can use Presumed (above that must use Real). Many foreign companies that aren’t on Simples use Presumed Profit because it’s more straightforward than Actual and often results in lower tax if you have decent margins.

-

Lucro Real (Actual Profit): This is the full regular regime required for large companies (and certain sectors like banks). Under Lucro Real, you calculate your net profit according to accounting principles and tax adjustments, and pay 15% IRPJ on that profit (plus 10% surtax on profit over R$240k/year), and 9% CSLL on profit. You also handle PIS/COFINS in a non-cumulative way (which means charging ~9.25% on gross revenue but you can deduct credits for certain costs – similar to a VAT). Lucro Real requires robust bookkeeping, monthly or quarterly tax calculations, and if you have a loss, you might pay minimal tax, but if you profit, you pay on actual amounts. It’s the most complex but the only option for some companies (e.g., if your business is a finance company or if you surpass the revenue threshold). Also, companies with very low profit margins might voluntarily choose Lucro Real, since any profit below the presumed percentages yields less tax than Presumido.

Simples NacionalChoosing the regime: When opening the company, discuss with your accountant which regime fits your projected size and activity. , if available, is usually best for small businesses due to significantly lower combined tax rates and bureaucracy. For instance, under Simples a small services company might pay ~6% of revenue in taxes at start, whereas under Presumed Profit it could be around 11–14%, and under Real Profit it could be up to ~34% of profit plus ~9% of revenue in PIS/COFINS. That said, Simples has its limits and some growing startups eventually outgrow it or are in activities not allowed.

Your accountant will formally register the company in the chosen tax regime with the authorities (Simples application or relevant tax office notices for Presumido/Real). If Simples is chosen, you’ll start filing the simplified PGDAS each month. If Presumed/Real, you’ll need to file DCTF, EFD, SPED accounting and other obligations – hence definitely requiring an accountant’s assistance.

Accounting Setup: Brazil’s law mandates that every company (except MEI) maintain contabilidade – official double-entry accounting records, even if you are a one-person company. You’ll need to hire an accountant (Contador) or an accounting firm. They will: - Register your company with labor and social security systems if you have or will have employees (e.g., Cadastro Esocial, INSS, FGTS employer registrations). - Handle your monthly bookkeeping, payroll, and tax calculations. - Issue required tax forms and pay taxes via DARF/GNRE/GPS as applicable. - Prepare annual financial statements (balance sheet, income statement) and corporate income tax returns (like the ECF – Escrituração Contábil Fiscal). - Ensure compliance with accessory obligations (there are many, such as SPED files, economic declarations, etc., depending on regime).

Given the complexity, allocate resources for accounting. Typical small-business accounting fees in Brazil might range from a few hundred to a couple thousand Reais per month depending on volume, but it’s money well spent to stay compliant. As one guide noted, “Accounting Services (monthly) $100 – $400” is a common cost range to budget.

CNPJ Opening Corporate Bank Account: Once the company is up and running in legal terms, you’ll want a business bank account in Brazil (Step 10 could be this, but it usually happens around this time). Banks will require your , the company’s constitutive documents, proof of registrations, and identification of the owners and representatives. The account opening can take a few days to a few weeks as banks do their compliance checks, especially for foreign shareholders. It helps if your Brazilian representative or a partner has a relationship with the bank. Having all required documents in hand (CNPJ certificate, Junta Comercial registration, CPF of owners, proof of address, etc.) will smooth the process. Large banks like Banco do Brasil, Itaú, Bradesco, Santander all handle foreign-owned accounts. There’s also Nubank and others, but some digital banks might not support corporate accounts for foreign entities yet.

Tip: Consult more than one bank to compare fees (some banks may demand higher minimum balances for companies with foreign owners). Also, note that to transfer money from abroad as capital, you’ll likely need the bank’s international department to guide you (they’ll code the incoming wire as foreign investment). After the account is open and funded, remember to do the Central Bank registration (previous step).

Step 10: Hiring Employees (Labor and Payroll Obligations)

{kind=link}

If you plan to hire employees in Brazil, you must comply with the country’s labor laws, which are quite extensive. First, as an employer, you need to: - Register the company with the Social Security Institute (INSS) and the FGTS (Guarantee Fund) systems. (Usually done by your accountant when the first hire is made.) - Set up payroll systems to handle monthly salaries, income tax withholding, social security contributions, and the mandatory 13th month salary and paid leave, etc. - Adhere to minimum wage and possibly higher floor wages if set by the industry or region.

Brazil uses an electronic labor system called eSocial where employers must report all events (hiring, terminations, monthly payroll, etc.). Your accountant will use eSocial to keep you compliant.

Key costs: Employers generally pay an additional ~28-30% on top of salaries in social charges (INSS employer part, FGTS 8%, etc.), and there are strong protections for employees (termination costs, etc.). Ensure you understand these or get guidance before hiring. Some businesses start with contractors (PJ) – i.e., hire other companies or individuals who bill you – but be cautious because if someone works like an employee, you can’t just call them a contractor without risk.

If you are a small operation without employees, you can skip this step. But note, even if you don’t hire employees, you as an owner could be on the payroll as a Pró-Labore (owner’s remuneration) which also triggers INSS contribution. Many foreign owners initially take profits only (which are tax-free in Brazil after corporate tax) rather than salary, but consult your accountant on best approach for compensation.

By now, if you’ve followed Steps 1–10, your business is legally established and ready to operate – you have all registrations (CNPJ, state, municipal), you have the necessary licenses to open your doors or launch your website, and you have an accountant to handle ongoing compliance. Congratulations, you can start doing business in Brazil! 🎊

CNPJCNPJBefore we move on to special topics, let’s summarize the typical timeline and costs for the process: - Timeline: If all documents are in order, foreign investors can incorporate entirely remotely and sometimes surprisingly fast. According to one 2025 report, in some cases business registration can be completed “in as little as 24 hours” under new digital systems, though that likely refers to receiving once documents are pre-prepared. A more typical timeline is 4–6 weeks to get everything done – factoring in time to gather/apostille documents, Junta approval, and additional registrations. Some sources still suggest 60–90 days for foreigners, especially if there are complications (like delays in document translation or obtaining licenses). In 2025, expect the core company registration (Junta + ) to be fairly quick (days to a couple weeks), and ancillary steps (licenses, bank account, etc.) to take a few more weeks. Always build in some buffer for unforeseen delays. - Costs: Official fees themselves aren’t very high (Junta Comercial fees, notary, etc., might sum to a few hundred USD). The bulk of cost can come from professional services and document prep. A law firm or consultancy package to open a company for a foreigner can range from $3,000 to $10,000 USD depending on complexity. This would include translations, notarizations, legal fees, and initial accounting setup. If you handle everything yourself (and have Portuguese fluency and knowledge to navigate), the out-of-pocket costs could be under $500 (this would be mainly fees and translations). Keep in mind ongoing costs: accounting services ($100–$400/month), perhaps a virtual office address service if needed, etc. And of course, the initial capital you invest is your own money but must be substantial enough if you’re pursuing an investor visa (e.g., R$500k). Budget accordingly for a smooth start.

Taxation and Accounting in Brazil: What Foreign Business Owners Must Know

{kind=link}

Brazil’s tax environment is known for its complexity – multiple taxes at federal, state, municipal levels – but with proper planning you can manage it and even benefit from simplified regimes.

Here’s a breakdown of key taxes and regimes:

-

Corporate Income Tax (IRPJ) and Social Contribution (CSLL): Together, these function like the corporate profits tax. The base rate is 15% on taxable income plus an additional 10% surtax on profits above R$240,000/year. CSLL is an additional 9% on profit. So effectively, under a standard regime a profitable company might pay 34% of its net profit in combined federal profit taxes. However, under Simples Nacional, these income taxes are folded into the single tax and come out to a much smaller percentage of revenue for small firms. Under Presumed Profit, the 15%+10% IRPJ and 9% CSLL are applied to presumed profit margins (as described earlier), often resulting in an effective rate much lower than 34% of actual profit (depending on margins). Under Actual Profit, you pay based on real profit at the full rates (but can offset losses from previous years up to 30%, etc.).

-

Tax on Gross Revenues – PIS/COFINS: These are federal contributions on gross revenue. In Simples, they’re included in the one tax. In Presumed Profit, PIS+COFINS are calculated on gross sales at combined 3.65% (cumulative system). In Actual Profit, they are non-cumulative at 9.25% but with credits for inputs (like a VAT). These are significant and often end up being a big tax cost for companies outside Simples. Again, many small businesses avoid this by qualifying for Simples where these are lower.

-

ICMS (Imposto sobre Circulação de Mercadorias e Serviços): A state-level VAT on goods and certain services (like transportation and communication). Rates range ~17% to 19% in most states (with some interstate rate differences and exceptions). If you sell physical goods or certain digital goods, you will encounter ICMS. Under Simples, ICMS is part of the single tax (for example, a small retailer under Simples might pay a total rate of 4-5% that includes ICMS). Outside Simples, ICMS is charged on each sale, and you can usually get credits for ICMS paid on inputs. It requires monthly filings per state.

-

ISS (Imposto sobre Serviços): A municipal service tax on services, generally 2% to 5% of service revenue, depending on the city and service type. For example, São Paulo and Rio often impose 5% ISS on most services. Under Simples, ISS is included in the single tax and at lower effective rates for small revenue. If not in Simples, service companies must collect and pay ISS to each city where services are provided. If you invoice clients in different municipalities, you may need to register in each of those or use the client’s ISS retention, etc. It can be complex if you have nationwide service sales.

-

Payroll Taxes: If you have employees, you’ll pay INSS employer contributions (~20% of wages) and other labor taxes (FGTS 8%, etc.). Simples companies get some breaks (Simples businesses don’t pay certain payroll taxes to entities like SEBRAE, SESI, etc.), but still pay INSS and FGTS.

Brazil also has a dividend exemption – profits after corporate taxes can be distributed to owners without further personal tax (as of 2025). This has made it common for owner-managers to take a modest salary (taxed via payroll) and the rest as dividends tax-free. Note: There are proposals to tax dividends in future tax reforms, but none enacted yet; keep an eye on legislative changes.

ICMS Upcoming Tax Reform: Brazil approved in 2023–2024 a major tax reform to simplify consumption taxes by creating a dual VAT (the CBS federal and IBS state) to eventually replace PIS, COFINS, , ISS, etc.. This will be phased in from 2026 onwards. While the exact impact is beyond this guide, the goal is to make things easier long-term. For now, anyone doing business in Brazil must contend with the current system – multiple filings – which underscores why having competent accounting support is vital.

Accounting and Compliance: By law, your company must keep accounting books and file various tax returns: - SPED Accounting and SPED Fiscal: electronic submissions of your accounts and tax calculations (for non-Simples companies). - DCTF: a federal tax debts declaration. - ECF (Escrituração Contábil Fiscal): annual corporate income tax return detailing profits and taxes. - ECD (Escrituração Contábil Digital): annual submission of your general ledger (if required, usually for larger companies or those under Real regime). - Simples companies file a simplified monthly DAS and an annual DASN-Simei (for MEI) or DEFIS (for Simples) declaring revenue.

Hire an Accountant: This cannot be stressed enough. As a foreign business owner, Brazilian accounting and tax reporting will likely be the most challenging aspect. A good accountant will ensure: - Your invoices (Notas Fiscais) are properly issued and recorded. - Your taxes are calculated correctly under your regime and paid on time (missing deadlines leads to fines quickly). - Your company books are kept in accordance with Brazilian GAAP (which is converging to IFRS for larger companies). - All those acronyms (DCTF, SPED, ECF, RAIS, DIRF, etc.) are handled.

In one foreign entrepreneur’s experience, failing to have a competent accountant from the start led to “registration errors in various agencies, tax and customs difficulties, and a company that couldn’t operate for 2 months”. She later had to fix those issues at great effort. So, see your accounting and compliance cost as an investment in peace of mind and longevity of your business.

Special Considerations for Digital Businesses (Online, Tech, SaaS, etc.)

{kind=link}

In the modern economy, many foreign entrepreneurs are interested in running digital businesses in Brazil – whether it’s an online service, a SaaS product, an e-commerce store, or a content creation platform. The good news is that the fundamental process of opening the business is the same as described above. But there are a few additional points to consider for digital enterprises:

-

No Physical Presence Required (but Address Still Needed): You might be able to operate an online business from anywhere, but Brazilian law still requires a registered local address for your company and often a local bank account for transactions in local currency. You might not need a storefront or office – many digital entrepreneurs use a co-working space or virtual office address to register the company. Make sure to check zoning – even home-based digital businesses may need to ensure their address is allowed for a business (some municipalities allow home offices for software/consulting companies without issue).

-

MEI and Small Digital Entrepreneurs: If you are a content creator, freelance programmer, or run a small online shop, you might qualify as an MEI (if you have residency). Many digital solopreneurs in Brazil use MEI because it covers numerous occupations (including “web designer”, “online sales”, “photographer”, etc.) and greatly simplifies tax to a small fixed amount. MEI is attractive for side hustles or testing a business concept online. Once revenue grows beyond the limit (R$81k/year currently) or if you need to take on partners, you’d transition to a normal company (Simples).

-

E-commerce (Physical Products): If your digital business involves selling physical goods through an online marketplace or store, you will have to deal with ICMS and shipping logistics. Brazil’s ICMS for e-commerce can be complicated by interstate tax split rules (difal). As a small e-commerce under Simples, the system handles a lot of it via the Simples DAS. Marketplaces like Mercado Livre or Amazon require you to have a CNPJ (if you’re doing it as a company) and to issue notas for sales. They sometimes facilitate tax collection for interstate sales. Ensure your accountant sets up the correct product codes (NCM) and that you understand postal requirements (e.g., including CPF/CNPJ of customers on shipments). Also, consider using fulfillment services if you’re overseas – but note that running a Brazil-based e-commerce from abroad is tough due to import costs; many foreigners instead partner with locals or drop-ship domestically.

-

SaaS and Export of Services: If you run a Software-as-a-Service or other online service that has customers outside Brazil, you should know about tax benefits for exports. Brazil generally does not tax export revenue for services – for example, ISS (municipal service tax) often is exempt when the service is provided to clients abroad (the rationale being the service is “consumed” outside Brazil). Also, PIS/COFINS on export revenues can be zero-rated. This means a tech startup in Brazil serving a global market might pay no ISS and no PIS/COFINS on its foreign sales (and just the corporate taxes on profits). You may need to provide documentation that funds received are from overseas for services performed (e.g., software development for a foreign client). Check the local municipal law – many follow the federal guidance of not taxing exports of services. This can make Brazil an interesting base for international-oriented digital businesses, potentially enjoying low tax on foreign income.

-

Local Sales of Digital Goods/Services: If your SaaS or app targets Brazilian customers, you will be subject to local taxes. Software and digital services taxation in Brazil has been a gray area – whether it’s ISS or ICMS. Recent consensus tends towards ISS for software services (with a few exceptions). So your SaaS fees to Brazilian clients likely incur ISS (2–5%). Some cloud or streaming services might be deemed communication services subject to ICMS. Also be aware of a special contribution called CIDE on remittances for technology or royalties (if you pay money out of Brazil for software licenses or tech services, a 10% CIDE might apply). For purely domestic digital sales, consider consulting a tax advisor to ensure you apply the correct tax. In the near future, the tax reform’s new VAT will unify this anyway.

-

Data Protection (LGPD): Running an online business means handling user data. Brazil has a General Data Protection Law (LGPD) similar to Europe’s GDPR. If you collect personal data (names, emails, etc.), you must comply with LGPD principles (obtain consent or have another legal basis, secure the data, etc.). Ensure your website/app has a privacy policy aligned with LGPD. Non-compliance can lead to fines, though enforcement is still ramping up.

-

Online Payments and Fintech: Brazil’s consumers often use local payment methods (boleto bancário, Pix instant payments, local credit cards). To accept these, you’ll integrate with a payment gateway or processor (PagSeguro, MercadoPago, Stripe Brazil, etc.). To set up those accounts, you’ll need your CNPJ and bank account. Fintech innovation is strong – Pix (an instant payment system) is ubiquitous now. Make sure to offer Pix for online sales – it’s easy once you have a bank account. If your business is fintech (like dealing with payment services or crypto), note that there are additional regulations and you might need licenses from the Central Bank or CVM depending on the model.

-

Tech Startup Incentives: Brazil has programs to encourage tech startups – for example, the government’s Startup Brasil initiative, various incubators and accelerators (some offer support to foreign-founded startups too). Some states have tax incentives for tech companies (often via reduction in ISS or providing grants for R&D). Research if there’s a tech park or incubator in your city – joining one might ease some bureaucratic processes and offer mentorship. Also, SEBRAE, the Brazilian Small Business Support Service, provides a lot of free or low-cost courses and consulting for new businesses – they even have tech-oriented programs. Even if materials are in Portuguese, as a foreigner you can avail of SEBRAE’s help for, say, refining your business plan or understanding compliance.

-

Digital VAT for cross-border services: Outside the scope of company registration, but worth noting: If you are a foreign company selling digital services to Brazilian consumers (without a local entity), Brazil charges a “Netflix tax” (ISS on imported service, or recently they talk of a digital services tax). But since you’re setting up a local entity, you’ll be charging Brazilian customers with local taxes as discussed.

In summary, a digital business in Brazil faces largely the same formation process as any other business. The differences emerge in the operational phase – dealing with possibly fewer physical permits (no brick-and-mortar concerns) but needing to navigate intellectual property, data, and an evolving digital tax landscape. Keep your accounting robust (digital or not, all companies file taxes!), and consider consulting specialized tech legal counsel for things like user terms, data policies, and any needed trademark registrations.

Brazil has a large and growing online market – e-commerce revenue is expected to hit $45 billion in 2025 – and also a thriving tech talent pool (over 475,000 tech graduates annually in Brazil). As a foreign tech entrepreneur, you can tap into this ecosystem. Setting up your company properly will enable you to hire local developers, contract Brazilian clients, and potentially qualify for Brazilian innovation grants or tax benefits.

Additional Resources and Downloads

{kind=link}

To complement this guide, here are some official resources and tools that can help foreign entrepreneurs navigating the process:

-

Ministério da Economia – Empresa Portal (): The Brazilian government’s portal for opening businesses (REDESIM). Contains step-by-step checklists (in Portuguese) and links to each state’s online registration system. Start at the page for Empresas or the specific Junta Comercial of your state.

-

Receita Federal – CNPJ and CPF Information: Official info on obtaining a CPF and registering CNPJ, including the online verification tool for CNPJs. The Receita site ( also has downloadable forms and manuals (in Portuguese).

-

Apex-Brasil (Trade & Investment Promotion Agency): ApexBrasil provides guidance to foreign investors, including sector opportunities and can assist with understanding incentives. They have English materials on doing business in Brazil.

-

SEBRAE: A resource for small business (mostly in Portuguese). They offer free courses on opening a business, including legal aspects and business plan writing.

-

Brazilian Consulate Websites: If you need a visa or CPF abroad, the consulate site for your country will have instructions and forms for CPF and investor visas. The Ministry of Foreign Affairs (Itamaraty) portal lists visa types and requirements (e.g., the investor visa requiring R$500k or R$150k for startups).

-

Downloadable Guide (PDF): We have prepared a comprehensive PDF guide consolidating this information in a more portable format, including checklists and a diagram of the registration process. (Download here: [link]). (This PDF includes a flowchart of the steps and a one-page checklist for quick reference.)

(If the PDF download link is not accessible in this text-only format, please refer to our website’s “Guide to Opening a Business in Brazil” section to download the PDF.)

Real-Life Case Studies: Successes and Lessons from Foreign Entrepreneurs in Brazil

To put all this information into perspective, let’s look at a couple of real-world examples of foreigners who navigated the process of starting businesses in Brazil. These cases illustrate the challenges and rewards of entrepreneurship in this country.

Case Study 1: Ksenia’s Café in Florianópolis

{kind=link}

Ksenia Balickaya is an entrepreneur from Russia who moved to Florianópolis, Brazil, and fulfilled her dream of opening a café and bakery. Ksenia’s café specializes in healthy breakfast foods and even introduced a product new to the local market – thin Armenian lavash bread – which she produces and sells. Her story sheds light on the ground-level challenges a foreigner can face:

-

Navigating Bureaucracy & Choosing the Right Advisors: Ksenia learned the hard way that you must choose your local accountant/consultant carefully. She initially hired a bookkeeper (“Antonio”) to help open the company, but he made numerous mistakes in the registration process. As a result, critical steps were left incomplete – her company wasn’t fully registered with all agencies, meaning it legally “could not function for 2 months” after the initial paperwork. Each time she discovered a missing registration (tax, customs, etc.), that accountant demanded extra fees. She later found out he was overcharging – “the cost for registering the company as an importer was 5 times the market rate, simply because I didn’t know the procedures”. Lesson: Do your homework and get second opinions. Unscrupulous providers might take advantage of a foreigner’s unfamiliarity. It’s wise to engage a reputable firm or get referrals from other expats.

-

Understanding Legal Requirements: Ksenia also encountered Brazil’s strict labor protections in a surprising way. When parting ways with that bad accountant, she had to be extremely cautious – in Brazil, even contractors can sometimes sue for perceived damages. She notes that local professionals “can take you to court if they feel they worked more than paid, and the law strongly protects workers – 95% of the time they win such cases”. She had to obtain written confirmation that neither party owed anything to safely terminate the service. This highlights how Brazil’s legal environment can be very different from elsewhere – one must document everything and follow proper procedures when ending contracts or employment.

-

Importing Equipment & Regulatory Hurdles: To support her café, Ksenia imported a special oven for baking lavash from abroad. This brought additional complexity: she needed to register her company as an importer with customs, get an import license for the equipment’s product code, and handle customs clearance. Because of earlier missteps in registration by her accountant, when the oven arrived at customs it was held up – the import code was initially not allowed and her company hadn’t been properly set up in the import system. She had to scramble to purchase a different import license and get a new customs declarant to resolve the issue. The oven eventually cleared, but it delayed her bakery production significantly. This underscores: if your business involves imports (bringing in equipment or products), factor in the extra layer of import/export regulations. You’ll need a RADAR license (importer’s license) and to follow Brazilian customs procedures. Many new foreign businesses might ignore this if they assume they can ship things in easily – not so, you must plan for it.

Despite the rocky start, Ksenia’s café did get up and running. She used the downtime to learn as much as possible about Brazilian tax and accounting rules herself, even writing a guide for friends to avoid the pitfalls she encountered. Her resilience paid off – by understanding the system better, she took control of her business. Now she runs a growing café and lavash production in Florianópolis, with an eye to scaling further in Brazil’s food industry.

Key takeaways from Ksenia’s experience: - Invest time in research and understanding local regulations, even if you have consultants. It will help you supervise their work and avoid being misled. - Choose reliable, referenced professionals to assist in company setup. Sometimes paying a bit more for a well-reviewed law firm or accountant is worth it. - Prepare for additional requirements if doing specific activities (like importing or dealing with health regulations for food). - Embrace learning: Ksenia turned her challenges into expertise that now saves her and others money and trouble.

Case Study 2: EBAC Online – A Russian Tech Startup Thriving in Brazil

{kind=link}

Not all foreign business stories in Brazil are cautionary tales – many are successes showing Brazil’s potential. One example is EBAC Online, an online creative arts and design school. EBAC (Escola Britânica de Artes Criativas) Online was launched in 2020 by Russian entrepreneurs Pavel Aleshin, Andrey Anishchenko, Alexander Avramov, together with Brazilian partner Rafael Steinhauser. They chose Brazil as the headquarters for this e-learning startup and it has flourished, attracting major investors and expanding across Latin America. By 2022, EBAC Online had raised about $12.5 million from venture funds including Baring Vostok and others – a significant achievement for a foreign-founded startup in Brazil.

What does the EBAC case illustrate? - Brazil as a Tech Market: The fact that Russian founders picked Brazil to launch a tech education platform underscores the opportunity they saw: Brazil’s huge population of young people eager to learn digital skills. Rather than launching in the overcrowded markets of U.S. or Europe, they identified a gap in Brazil and localized their product for Portuguese-speaking audiences. The startup’s success (future “unicorn” potential per Forbes Russia) shows that foreign founders can indeed tap into Brazil’s growing demand for tech services and education. - Local Partnerships: The inclusion of a Brazilian co-founder (Steinhauser) likely helped navigate local business culture and networks. This is a common success factor – while 100% foreign ownership is allowed, having a local partner or key hires who understand the Brazilian market can accelerate growth and help avoid pitfalls in operations. - Leveraging Incentives: Although not detailed in the snippet, a startup like EBAC could leverage some of Brazil’s innovation incentives. The government’s focus on tech (from startup visas for founders to programs like PEIEX for exporters or tax breaks for tech investments) can be advantageous. Also, foreign-led startups often benefit from local accelerators (e.g., Cubo Itaú, Endeavor, etc., many of which welcome foreign founders). - Persistence in Bureaucracy: It’s not public, but surely EBAC’s team had to go through the same steps – CPF, CNPJ, etc. – that we discussed. The difference is they were likely well-advised (perhaps by venture attorneys) and capitalized enough to hire top legal/accounting help. When aiming big (raising millions), one can’t afford compliance mistakes. This suggests if you have a high-growth startup idea, it’s worth investing in top-tier legal counsel in Brazil to set up correctly from day one (structure, intellectual property, employment contracts, etc. in place).

Today, EBAC Online is headquartered in São Paulo (the hub of Brazil’s startup scene) and is expanding regionally. It stands as proof that foreign entrepreneurs can not only start a business in Brazil but scale it successfully, given a strong value proposition and adaptation to the local market.

Key takeaways from EBAC’s success: - Brazil’s large market can catapult a startup to scale quickly – especially in tech and online sectors where user bases grow fast. - Adapt to local needs: EBAC did an online education platform tailored to Brazilian learners. For you, whatever your business, localize your offering (language, preferences, pricing model, etc.). - Work within the system: Comply with regulations, but also use government programs that exist to help (they had Brazilian leadership and likely used local grants or connections). - Networking: São Paulo’s tech ecosystem is vibrant. Engaging with local startup communities (meetups, investor events) as a foreign founder is crucial – it’s a smaller world than, say, Silicon Valley, and people are very welcoming to foreign innovators, given Brazil’s hunger for tech solutions.

Case Study 3: (Hypothetical) Roberto’s IT Consulting in São Paulo

(While not drawn from a single published story, this composite case reflects common experiences of foreigners, including Russians, who have opened small IT or consulting businesses in Brazil.)

“Roberto” is a software developer from Russia who moved to São Paulo and started a boutique IT consulting firm. He set up a Sociedade Limitada with one Brazilian friend as a minor partner (mainly to have a local administrator while Roberto was waiting on his investor visa). The business provides custom software development services for Brazilian companies.

-

Roberto opted for Simples Nacional As an LTDA with himself (foreign individual) and a Brazilian partner, the company was eligible. This kept his taxes low – roughly 6% on revenues initially – and compliance straightforward, managed by a part-time accountant. He noted that if he had instead opened the company as a wholly foreign-owned subsidiary of his existing overseas company, he wouldn’t have gotten Simples status. By registering personally, he saved significantly on taxes. This highlights the benefit for small foreign entrepreneurs to own the business directly as individuals rather than through a foreign holding entity, at least until the business grows.

-

One challenge Roberto faced was the language and cultural barrier in business settings. Negotiating contracts in Portuguese and understanding Brazilian clients’ expectations took some adjustment. He took intensive Portuguese classes and hired a bilingual sales representative to help interface with clients. For legal contracts, he invested in professional translations to ensure nothing was lost in translation. Brazil operates in Portuguese, so foreign founders must adapt linguistically for day-to-day operations, even though many educated Brazilians speak English.

-

Roberto’s IT firm benefited from Brazil’s abundant tech talent. He was able to hire two junior developers from the local university at competitive salaries. However, he had to quickly learn Brazil’s labor laws; for instance, he discovered that the cost of an employee is about 70% on top of their salary when including taxes, benefits, paid vacations, 13th salary, etc. To keep flexible, he initially engaged some freelancers (who had their own CNPJs as PJs) instead of full employees – a common practice in Brazil’s IT sector. Still, after a year, he transitioned them to full employment to build a stable team, accepting the higher cost but avoiding any risk of labor misclassification issues. This underscores the need to plan for HR compliance even in a small startup.

-

Networking was key. Roberto joined a local startup incubator and attended industry meetups (including ones for Russian expats in tech). Through these, he landed a couple of major contracts. The Brazilian business culture relies a lot on relationships and trust – being present in São Paulo and making personal connections was crucial to establish credibility as a newcomer.

After two years, Roberto’s consulting firm grew and even started serving a client in the United States from Brazil. Thanks to Brazil’s policies, the payment from the US client for export of services came in free of certain taxes, and he could legally keep the dollars or convert at a good rate. He registered those incoming funds properly as export revenue, which helped avoid any tax on that portion (since ISS was not charged on exports in his city).

Today, Roberto’s small company is thriving, and he is even considering bringing more Russian IT professionals to Brazil under work visas, tapping both into Brazil’s local talent and his overseas connections. His story reflects that while bureaucracy is challenging, Brazil’s market and resources can be very rewarding for those who persist.

Key takeaways from Roberto’s (composite) experience: - Language & cultural adaptation is important – invest in it early (learn Portuguese, understand Brazilian business etiquette). - Structure your business in a way to maximize tax benefits (e.g., Simples) if you’re small – minor tweaks in setup can have big tax implications. - Be mindful of labor laws – use probation periods, consider outsourcing carefully, but ultimately comply with the protections in place. - Network: leverage both expat and local networks. Foreign entrepreneurs often find support in communities of fellow expats and must integrate into local industry circles.

Each of these cases – the café owner, the tech startup founders, the IT consultant – teaches us something about opening and running a business in Brazil. There will be bumps in the road, but as these entrepreneurs show, it’s possible to overcome them and succeed in very different industries.

Conclusion

Starting a business in Brazil as a foreigner is a journey that requires preparation, patience, and adaptation – but it is certainly achievable, and many foreigners are thriving as business owners in Brazil today. In this guide, we’ve covered the step-by-step process – from pre-requisites like CPF and a local representative, through legal incorporation (Junta Comercial, CNPJ), obtaining licenses, to setting up taxes and ongoing compliance. We also discussed specialized topics like digital businesses, and heard insights from real entrepreneurs who have been in your shoes.

Here are a few final best-practice tips to keep in mind:

-

Plan and double-check requirements at each step. Use checklists (like the one in our PDF guide) so nothing falls through the cracks. Brazilian bureaucracy is unforgiving on missing documents.

-

Leverage professional help, but stay informed. Hire a trustworthy accountant and/or lawyer, especially to get started. But also educate yourself (hopefully this guide has helped) – knowledgeable business owners can steer their helpers and catch errors.

-

Be compliant, but also proactive. Meet all obligations (register that investment, file those taxes on time) – non-compliance can result in heavy fines or even business suspension. At the same time, seek out incentives: tax benefits, incubation programs, financing options from BNDES (the development bank) or grants – Brazil has support for businesses that you shouldn’t leave on the table.

-

Cultural integration: learn the language, respect the local way of doing business (which might favor in-person meetings, building trust over coffee before jumping to contracts, etc.). This will not only help avoid miscommunication but also endear you to clients, partners, and officials.

-

Stay resilient and patient. Processes can be slow or seem convoluted, especially if you’re used to a more streamlined system. For example, opening a bank account might require more paperwork and time than you expect; licenses might take longer in one city than another. Bureaucracy is part of the game – those who succeed are those who persist and find a way through the red tape. As the saying goes, “Brazil is not for beginners”, but once you get through the initial setup, you’ll find day-to-day operations become routine.