Foreigners can usually open a Brazilian bank account once they have a CPF; digital banks are usually the fastest route for new arrivals.

Brazilian tax exposure changes sharply once you become a tax resident, because worldwide income generally enters the picture.

Finance and Taxation in Brazil for Expats – Comprehensive Guide

Disclaimer: This article is for informational purposes only and not legal or financial advice. Brazil’s regulations change frequently; always verify current requirements with official sources and professional advisors.

Quick answer

Related reading: Finance & Taxation | Work & Business | Visa Requirements | Q&A

Foreigners can usually open a Brazilian bank account once they have a CPF; digital banks are usually the fastest route for new arrivals.

Brazilian tax exposure changes sharply once you become a tax resident, because worldwide income generally enters the picture.

Inbound transfers are usually easier and cheaper than outbound transfers, so IOF, FX spread, and documentation should be checked before moving large sums.

Most costly mistakes are practical, not theoretical: delaying the CPF, using only foreign cards, missing tax deadlines, and failing to formalize final departure.

Use this guide to make decisions in the right order: banking setup first, transfer mechanics second, tax residency third, and departure planning before you leave.

| Topic | Fast answer |

|---|---|

|

Bank account |

CPF + passport + a Brazilian address are the usual starting point; digital banks are typically the easiest first step. |

|

Tax residency |

Many expats become Brazilian tax residents after more than 183 days in Brazil in a 12-month period, though some long-term entry scenarios can trigger residency earlier. |

|

Foreign income |

Once resident, Brazil generally taxes worldwide income, with foreign tax credits or treaties used to reduce double taxation where available. |

|

IOF |

This guide uses the common planning benchmarks already discussed in the article: lighter inbound FX taxation and materially higher outbound personal remittance taxation, subject to the exact transaction category. |

|

Departure |

A clean tax exit normally requires both the communication of departure and the final departure return. |

Finance and Taxation in Brazil — Quick Start PDF

Premium quick-start guide for expats: CPF, banking, transfers, tax residency, first filing, and a clean financial exit

Download the PDF Guide: Finance and Taxation in Brazil - Quick StartTable of Contents

Use the links below to jump directly to the section you need.

Introduction

Related reading: Work & Business | Finance & Taxation | Guide to Moving to Brazil | Cost of Living

Moving to Brazil as an expat brings exciting opportunities – but also new challenges in managing your finances and taxes. Brazil’s banking system, currency controls, and tax rules can differ greatly from what you’re used to. This comprehensive guide will walk you through every aspect of finance and taxation for foreign residents in Brazil, from opening a bank account and transferring money, to handling currency exchange, income taxes, and legal obligations. We’ll cover how to open a bank account as a foreigner, use Brazil’s modern payment systems, minimize fees when moving money, and comply with Brazilian tax laws (including income tax filing, double taxation treaties, and procedures when you leave Brazil) – all with practical examples, checklists, and step-by-step instructions. Our goal is to equip you with the knowledge to manage your money confidently in Brazil while avoiding common pitfalls.

What you’ll learn in this guide:

- Banking in Brazil for Foreigners: Why you need a local bank account, how to get a CPF (Brazilian Tax ID), and step-by-step instructions to open accounts (digital vs. traditional banks). We compare major banks and highlight Brazil’s instant payment system (PIX) that every expat should use.

- Transferring Money & Currency Exchange: The best ways to send money to and from Brazil, how to get favorable exchange rates, understanding Brazil’s currency (the Real), and important regulations (like the IOF financial tax and cash carry limits).

- Income Tax in Brazil for Expats: Who counts as a tax resident, how foreign income is taxed, Brazil’s income tax rates and filing process, key deadlines, and how to avoid double taxation using treaties or credits. We’ll also explain what financial declarations you may need to file (such as declaring foreign assets) and how to handle taxes when you depart Brazil

- Other Taxes and Obligations: Overview of other taxes expats should know – from social security contributions to property taxes – and how Brazil’s tax system compares to other countries.

- Common Mistakes to Avoid: A special section on frequent errors (like failing to get a CPF, missing tax deadlines, or paying unnecessary fees) and how to stay compliant and financially savvy.

- FAQs and Resources: Answers to frequently asked questions and references to official sources and expert tips.

By the end of this guide, you’ll have a clear roadmap for managing your finances in Brazil – whether you’re working locally, retiring abroad, or remotely working for a foreign employer. Let’s dive in and demystify Brazil’s finance and tax system for expats!

(Note: All information is up to date as of early 2026, with recent legal changes incorporated. Always double-check current laws as Brazil updates regulations frequently.)

Banking in Brazil for Foreigners

Related reading: Finance & Taxation | Local Bureaucracy | Work & Business | Remote Work in Brazil

Can foreigners open a bank account in Brazil? Short answer: yes. In practice, a CPF, passport, and a usable Brazilian address are usually the minimum starting point, with digital banks typically being the easiest route for new arrivals.

Section summary

Start with the three essentials: get a CPF, open a practical local account, and activate PIX. Most readers should treat traditional banks as a second-step option unless an employer, payroll setup, or product requirement forces a branch-based account.

Having a Brazilian bank account is practically essential for anyone planning an extended stay in Brazil. Without one, everyday tasks like paying rent, utility bills, or even buying groceries can become complicated and expensive. In this section, we’ll cover how Brazil’s banking system works, what you need to open an account as a foreigner, and why a CPF number is your golden key. We’ll also compare digital vs. traditional banks, introduce a new option for non-resident accounts, and provide a checklist to get you started.

Summary box — banking setup in Brazil

- Get the CPF early; it unlocks banking, PIX, contracts, and most practical financial tasks.

- Digital banks are usually the fastest opening route for new arrivals; branch banks can still matter for complex services or employer requirements.

- Proof of address is often the first practical bottleneck, so solve it early instead of at the bank counter.

- If you are not yet living in Brazil, check whether a non-resident account route is available bank-by-bank before assuming you must wait.

Brazilian Currency and Banking Overview

Related reading: Finance & Taxation | Cost of Living | Work & Business

Brazil’s currency is the Real, abbreviated BRL and symbolized as R$. It’s a free-floating currency, meaning its value fluctuates according to the market. In recent years, the exchange rate has hovered around R$5 per US$1 (though it varies), so it’s important to keep an eye on exchange rates when moving money. The Real is a decimal currency (100 centavos = R$1). You’ll encounter banknotes in denominations from R$2 up to R$200, and coins from R$0.05 (5 centavos) to R$1. Brazil has a history of inflation, but in the past decade inflation has been moderate; nevertheless, interest rates tend to be high by international standards (which affects loans and savings).

{kind=link}

Banks in Brazil: The country has a mix of large traditional banks and a new wave of digital banks. The banking sector is heavily regulated by the Central Bank of Brazil (Banco Central do Brasil), which ensures stability and protection for depositors. As a foreigner, you can open a bank account in Brazil – either a normal resident account (if you have local documentation) or a special non-resident account if you’re not living in Brazil (more on that soon). Having a local account is crucial because Brazil is a largely cashless society in practice – Brazilians frequently use electronic payments for everything thanks to modern systems like PIX (an instant transfer system) and boletos (payment vouchers). Many merchants and service providers expect payments via local methods. Without a Brazilian account, you would rely on foreign credit cards or cash, incurring steep foreign transaction fees (5–8% per purchase when including exchange markups).

Why You Need a Local Bank Account: Aside from avoiding foreign card fees, a local account lets you use PIX (free instant transfers 24/7) and pay bills via boleto (barcode slips common for rent and utilities). Many landlords and employers will require a Brazilian bank account to send or receive payments. You’ll also get access to better exchange rates through services integrated with local banks (like Wise or local remittance companies). Finally, Brazil often offers discounts for cash or PIX payments (5–15% off vs credit card prices), so a local account can literally save you money daily.

Real-world example: Sarah moved to Brazil and tried to manage with her US bank card. She quickly found that her bank charged 3% foreign transaction fees, Brazilian ATMs charged withdrawal fees, and many smaller shops only accepted PIX or local debit cards. After a month, she opened a local bank account, got a debit card, and started using PIX – immediately saving money on fees and even getting a 10% discount on her rent for paying via bank transfer instead of international wire.

CPF – Your Key to Financial Access in Brazil

Related reading: Local Bureaucracy | Visa Requirements | Q&A

{kind=link}

The CPF (Cadastro de Pessoa Física) is a Brazilian taxpayer identification number. It is absolutely mandatory for virtually all financial (and many non-financial) activities in Brazil – including opening a bank account, signing a lease, getting a mobile phone plan, or even shopping online in some cases. If you don’t have a CPF, obtaining one is your first step. There are no exceptions: even non-resident foreigners must have a CPF to open accounts or invest in Brazil.

What is a CPF? It’s an 11-digit individual tax ID, similar to a Social Security Number in the US or a National Insurance number in the UK. The CPF is issued by the Brazilian Federal Revenue (Receita Federal) to Brazilians and foreigners alike. For Brazilians, it’s often issued at birth or when turning 18. As a foreigner, you can apply for a CPF even if you don’t have residency yet – in fact, many get it while on a tourist visa so they can set up practical things like a bank account or utilities.

How to get a CPF: You can apply in Brazil at a Banco do Brasil, Caixa Econômica, or Correios (post office) branch by filling a form and showing your passport; there’s a small fee (~R$7). You’ll then finalize the registration at a Receita Federal office (tax office) with your documents. If you’re not in Brazil yet, you can apply at a Brazilian consulate abroad – often this involves emailing forms and copies of ID, then picking up the number. The CPF itself is just a number; you can print a certificate (Comprovante de Inscrição no CPF) from Receita Federal’s website once issued. For a detailed walkthrough, see our Guide on Obtaining a CPF (we provide step-by-step instructions, required documents, and tips).

Why CPF matters: Without a CPF, banks will not even consider your application. You’ll also use your CPF as your identification for credit history, for any tax filings, and when you register for utilities, loyalty programs, medical services, etc. Think of it as your “financial passport” inside Brazil. Memorize your CPF number and keep the proof of registration handy for paperwork.

Checklist: Getting Your CPF

-

Valid Passport: You’ll need your passport (and a copy) for identification.

-

Brazilian address (if applying in Brazil) or your home address (if

abroad).

It’s okay if you’re staying at a friend’s or hotel – you can use that

address.

-

Application form: Fill out the CPF request form (online or at the place of

application). If at a

consulate, follow their specific process.

- Fee payment: Pay the small fee (if

applying in

Brazil, pay at the bank/post office when you apply). Keep the receipt.

- Tax office

visit: In

Brazil, take the receipt to a Receita Federal office to finalize and receive your CPF number (often

issued on the

spot). Abroad, the consulate will coordinate issuing the number.

- Print CPF

confirmation:

Once you have the number, go to Receita Federal’s website and print your CPF enrollment

certificate. This

serves as proof when opening accounts.

(Note: You donotneed to be a resident

or have a

visa to get a CPF – tourists can get one. But you do need aCPFto become a

resident (for

visas) and for almost everything else!)

Types of Bank Accounts: Digital vs. Traditional Banks

Related reading: Finance & Taxation | Employment in Brazil | Remote Work in Brazil

{kind=link}

Brazil’s banking landscape has transformed in the last decade with the rise of fintech and digital banks. As an expat, you have two main paths to open an account:

- Digital banks (online-only) – e.g. Nubank, Banco Inter, C6 Bank, etc.

- Traditional banks (brick-and-mortar) – e.g. Banco do Brasil, Itaú, Bradesco, Santander, Caixa.

Digital Banks: These are app-based banks with no (or very few) physical branches. They have exploded in popularity – over 100 million Brazilians now use digital banking. For foreigners, digital banks are usually the fastest and easiest option. Many digital banks accept foreigners with just a CPF and passport, and you can apply through the bank’s smartphone app without visiting a branch. They often have no monthly fees, free basic services, and user-friendly apps (some offer English language interface). Digital banks are great for everyday banking: receiving salary, making PIX transfers, paying bills, and using a debit card. However, they might not offer more complex services like international wire transfers (some do, like Inter, which offers some international transfer options).

Traditional Banks: These include large established banks and typically require you to visit a branch in person to open an account. They may have monthly maintenance fees (ranging ~R$20–60 depending on account tier). Traditional banks do accept foreigners but often require more documentation (like proof of address in Brazil and proof of income) and the process can take 1–2 weeks. Approval can sometimes depend on the individual branch manager’s familiarity with opening accounts for foreigners – experiences vary, which means if one branch turns you down, trying a different branch or banker might succeed. Traditional banks might be necessary if, for example, your employer requires payroll at a specific bank or you need services like a checkbook, a credit card with a higher limit, or certain investment products not available through fintechs.

Here’s a quick comparison of popular banks for expats, and their features:

Bank Options for Foreigners in Brazil:

| Bank | Type | Foreigners Allowed? | Monthly Fee | Notable Features |

|---|---|---|---|---|

|

Nubank |

Digital |

✓ Yes (CPF + passport) |

Free |

Easiest approval for foreigners; intuitive app in English; free debit + credit (on approval) |

|

Banco Inter |

Digital |

✓ Yes |

Free |

Free international transfers (limited); multi-currency support (USD/EUR accounts) |

|

C6 Bank |

Digital |

✓ Yes |

Free |

Offers USD/EUR accounts; robust platform for investments; points program |

|

Bradesco |

Traditional |

✓ Yes (varies by branch) |

~R$30–50/mo * |

Very large network; some employers insist on Bradesco; full-service banking (loans, etc.) |

|

Itaú |

Traditional |

✓ Yes (varies) * |

~R$30–60/mo * |

Largest private bank; many branches/ATMs; good online banking (Portuguese only) |

|

Banco do Brasil |

Traditional (government-run) |

✓ Yes (varies) * |

~R$25–50/mo * |

Government bank – useful if you need to pay taxes or use govt services; English online banking option in some cases |

|

Santander |

Traditional |

✓ Yes |

~R$30–60/mo * |

International presence (if you have Santander abroad, might help); often has staff for expat accounts in big cities |

|

Caixa |

Traditional (government) |

✓ Yes (slower) |

Low/Free for basic accounts |

Government savings bank – useful for FGTS, social payments; not very expat-focused, process can be bureaucratic. |

(✓ Yesmeans these banks have been known to open accounts for foreigners.

“Varies” indicates

it’s allowed in policy, but branch discretion applies. )

Monthly fees can often be

waived if

you maintain a minimum balance or if you choose a basic limited-service account. Brazilian law requires

banks to

offer a fee-free basic checking account (Conta de Serviços Essenciais) with limited monthly

transactions

– ask about this if you won’t do many transactions.)*

As shown above, digital banks are typically the first choice for newly arrived expats due to zero fees and quick setup. Traditional banks come into play for specific needs. Many expats actually maintain both: a digital bank for day-to-day use and a traditional bank if required for salary or to access a wider ATM network or services.

Insight: Brazil’s embrace of digital banking means even newcomers can get an account within a day. In contrast to some countries where proof of residency might be required, Brazilian fintech banks often only ask for a Brazilian address (which could be temporary) and your documents. This is a big improvement from a decade ago, when opening an account as a foreigner could be quite difficult without a resident ID. Now, an expat with a CPF can become fully banked in Brazil with just a smartphone.

Step-by-Step: Opening a Bank Account as a Foreigner

Related reading: Finance & Taxation | Local Bureaucracy | Employment in Brazil

{kind=link}

Now let’s get practical. Below is a step-by-step walkthrough focusing first on the recommended digital bank route, followed by notes on the traditional bank process if you need it.

- Opening a Digital Bank Account (example: Nubank) – approx. 15–30 minutes application time, 1–2 days for approval.

- Download the App: Go to the App Store or Google Play and download the app of the bank (e.g. Nubank, Inter, C6). The app will guide you through the account opening process. Ensure your phone is set to allow the app access to camera, etc., for verification steps.

- Register with Personal Details: Open the app and start a new account registration. You’ll be prompted to enter your CPF number, full name (make sure it exactly matches how it appears on your CPF record or passport), date of birth, email, and a Brazilian phone number. (Tip: a prepaid SIM card is fine for the phone requirement. You just need a local number for verification codes.)

- Provide ID Documents: Select the ID type you will use. For foreigners, choose Passport. You’ll typically need to take a photo of your passport photo page within the app. Ensure the photo is clear with all text legible (good lighting, flat background) – the app uses OCR to read your info.

- Selfie Verification: The app will ask for a selfie or short video to verify your identity. Follow the on-screen instructions (usually, remove glasses, look at camera in good light, etc.). This is a standard KYC (Know Your Customer)

- Enter a Brazilian Address: You must input a local mailing address in Brazil. This could be your apartment, a friend’s place, or even a hotel/hostel if you’re new (courier delivery of your debit card will go here). You do not typically need to upload a proof of address for digital banks – just provide the address.

- Submit and Wait for Approval: After submitting, you’ll see a confirmation. Most digital banks will process your application in 24–48 hours for foreigners. Some lucky applicants get almost instant approval. If additional documents are needed, you’ll be notified in-app or by email.

- Account Activation: Once approved, you’ll receive an email or app notification. Your digital account (with an account number and agency number) is now active, and you can start using it immediately via the app – even before your physical debit card arrives. Notably, PIX will be active immediately: you can generate PIX keys like your CPF or email to receive transfers, and start sending money via PIX.

- Receive Debit Card: The bank will mail a physical debit card to the address you provided, usually within 1–2 weeks. This is useful for ATM withdrawals and card purchases. But you don’t have to wait for it – you can use the app for transfers and bill payments right away. Some digital banks also provide a virtual card in-app for online shopping while the physical card is en route.

If your application is rejected – don’t panic. It can happen if the bank couldn’t verify some information or if they have a policy about certain visa types. Commonly, waiting a week and reapplying works, or you can try an alternative digital bank. For instance, if Nubank said no, try Banco Inter or C6, which might have different criteria. Many expats report Nubank has a high success rate for first attempts.

- Opening a Traditional Bank Account (In-Branch) – if required by employer/landlord or for services a fintech can’t provide.

- Choose a Bank and Branch: Ideally, go to a larger branch in a major city or expat-friendly area; staff there are more likely to have experience with foreign clients. Public banks like Banco do Brasil might have an international desk in cities like São Paulo or Rio. Private banks (Itaú, Bradesco, Santander) also can serve foreigners. It’s wise to bring a Portuguese-speaking friend if you’re not comfortable in Portuguese, as not all bank staff speak English.

- Documents to Bring: You will almost certainly need: Passport (original + copy), CPF (proof of enrollment), Proof of Brazilian address (e.g. utility bill or rental contract with your name; if you only have a temporary address, explain your situation – some banks accept a declaration from the person you’re staying with), and Proof of income (such as a payslip, an employment contract, or even last year’s tax return from your home country). If you have a Brazilian ID card for foreigners (RNE/CRNM) or at least the protocol, bring that too – it’s not mandatory if you don’t have it yet, but it helps. Also be prepared to provide a Brazilian phone number and email for contact.

- Initial Deposit: Some banks may ask for a minimum opening deposit (varies by bank/branch, often R$50–R$200). It’s good to have some cash on hand for this or be ready to transfer once the account is open.

- At the Branch – Application: Inform the receptionist you want to open a “conta corrente” (checking account) and that you are a foreign resident. They will direct you to the appropriate manager or desk. Present your documents. You’ll fill out or sign an application form. They will enter your info into their system. Tip: Emphasize that you have all required documents; if one branch seems unsure, sometimes politely mentioning that other foreigners have opened accounts with just passport/CPF/address at their bank might encourage them to check their policy. Each bank’s policy is slightly different, but all require CPF and passport at minimum.

- Account Setup and Card: The account might not be active immediately – often, it takes a few days for approval (they might need headquarters to validate foreign documents). The bank will contact you (email/phone) when the account is ready, or they’ll give you a slip with account details if issued on the spot. Your debit card (cartão) typically is mailed to your address or available for pickup at the branch in about a week. The branch will let you know the procedure.

- Online Banking: The banker will help you register for online banking and set up a password/pin. Brazilian banks usually have you create an internet banking username and a PIN, and you’ll get a physical or SMS token for additional security on transactions.

- Ready to Bank: Once fully active, you can deposit funds, set up PIX (with your CPF, phone, or email as keys), and operate the account. Do note that traditional banks might have limits on transfers for new accounts initially and using the mobile app might require activating the device at an ATM first (the bank staff will explain if needed). Also, ask about fees: ensure you know your account’s monthly fee and what it includes (number of free transfers, etc.), and how to avoid extra charges.

Documents Summary for Traditional Banks: To recap, typical requirements: Passport + Visa, CPF, Proof of address in Brazil, Proof of income/employment, Brazilian phone number, possibly your foreign ID card if you have one.

Common Hurdle: Proof of address can be tricky if you just arrived. If you’re staying at a hotel or Airbnb, you won’t have a utility bill in your name. In such cases, some banks accept a letter from the hotel or an Airbnb receipt. Another solution is to change your foreign driver’s license address to your Brazil address if that’s accepted (not common). Often, expats use the address of a friend or employer. In some cases, banks will allow opening with just the passport and CPF and let you update address proof later – this depends on the manager. Digital banks don’t usually ask for an address document at all, which is why they’re easier as a first step.

New Option: Non-Resident Bank Accounts (CND)

Related reading: Residency by Investment | Finance & Taxation | Guide to Moving to Brazil

{kind=link}

What if you want a Brazilian bank account but you’re not (or not yet) living in Brazil? Perhaps you’re an investor abroad or planning a move but not a resident. Historically, opening an account as a non-resident was extremely difficult, involving lots of bureaucracy (you needed a Brazilian legal representative and every transfer was treated as a foreign exchange transaction).

Good news: As of January 1, 2025, Brazil updated its regulations to make non-resident accounts much more accessible. The Central Bank and CVM (securities regulator) issued Joint Resolution No. 13/2024, modernizing the Conta de Não Residente (CNR or CND) – the official non-resident Brazilian Real account.

What is a CND? It stands for “Conta de Não Residente” – a bank account in Brazilian reais that can be opened by individuals or companies who do not reside in Brazil for tax purposes. In practice, it allows foreigners abroad (or Brazilians who moved overseas) to hold an account in Brazil. The account is denominated in BRL and lets you receive and send funds within Brazil, invest in Brazilian assets, and convert currency through the account.

Key features of the new CND rules:

- Simplified process: Less bureaucracy than before. No legal representative in Brazil is required for individuals using their own funds (previously you had to appoint a Brazilian resident to represent your account).

- Less forced currency exchange: You can keep funds in BRL and transact without each operation being treated as a separate FX deal, which lowers costs and delays.

- Investments allowed: You can use a CND to invest directly in Brazilian financial assets and securities (stocks, bonds, etc.), which previously required separate registration.

- Stability: If you later move to Brazil and become a resident, you don’t have to close the account – it can be converted to a resident account, avoiding disruption.

- Transparency: Banks have record-keeping obligations (10 years) for oversight, which is on them, not you.

Who can open a CND?

- Individuals living abroad (foreigners with no Brazilian tax

residency,

or Brazilian nationals living overseas).

- Foreign companies wanting a Brazilian

account.

Conditions: Use your own funds (personal money, not on

behalf of

others). There are also transaction limits for certain simplified treatment –

e.g. up to

BRL 2 million per month per financial institution for some exemptions (this mainly

affects very

large transfers; typical users won’t hit this).

In essence, a CND allows a non-resident to plug into Brazil’s banking system almost like a local, which is great for managing Brazilian investments or preparing for a move. For example, an expat not yet in Brazil can open a CND, transfer money into Brazil and convert to BRL at better rates, then have funds ready for use (to buy property, etc.) once they arrive – all legally and in a transparent way.

How to open a CND: The rules changed at the regulatory level, but implementation is bank-by-bank. Not all Brazilian banks may immediately offer CND accounts to individuals without hassle – you might need to find a bank that actively markets this service (some banks or brokers that cater to foreigners likely will). The process will involve proving your identity (passport) and obtaining a CPF (yes, you still need a CPF even as a non-resident to open the account) since CPF is required for any account. You’ll also declare you’re non-resident. It might be wise to contact the international/private banking unit of a major bank or a Brazilian investment platform that works with expats. As 2025 progresses, expect more streamlined online methods for this.

Benefits of a CND:

- Direct access to Brazil’s

high-interest savings

and investment options, even while abroad (Brazil’s interest rates on certain deposits can be

attractive).

- Diversification: Hold part of your money in BRL, which can be

beneficial if

you anticipate currency moves or just want to diversify assets geographically.

- Ease of

eventual

move: If you plan to move to Brazil later, you already have a local account set up; if you

plan to

leave Brazil, you can keep your account as non-resident without closing everything.

- Tax

optimization: While you’ll pay Brazilian tax on any Brazil-sourced earnings (like

interest) in

the account, you might avoid certain transactional taxes because of the new rules, and you can take

advantage of

double taxation treaties for investment income if applicable.

Important: Even with simplification, CND holders must still comply with all KYC/AML (anti-money laundering) requirements. That means disclosing the purpose of the account, expected flow of funds, etc. Large transfers will still need justification (own funds, etc.), and your home country may tax any income you earn in Brazil through the account, so you need to consider international tax implications. Always declare the existence of this account if required in your home country (e.g. US citizens need to report foreign accounts).

Using Your Brazilian Bank Account

Related reading: Finance & Taxation | Cost of Living | Remote Work in Brazil

{kind=link}

Once you have an account, here are a few key Brazilian banking tools/quirks to know:

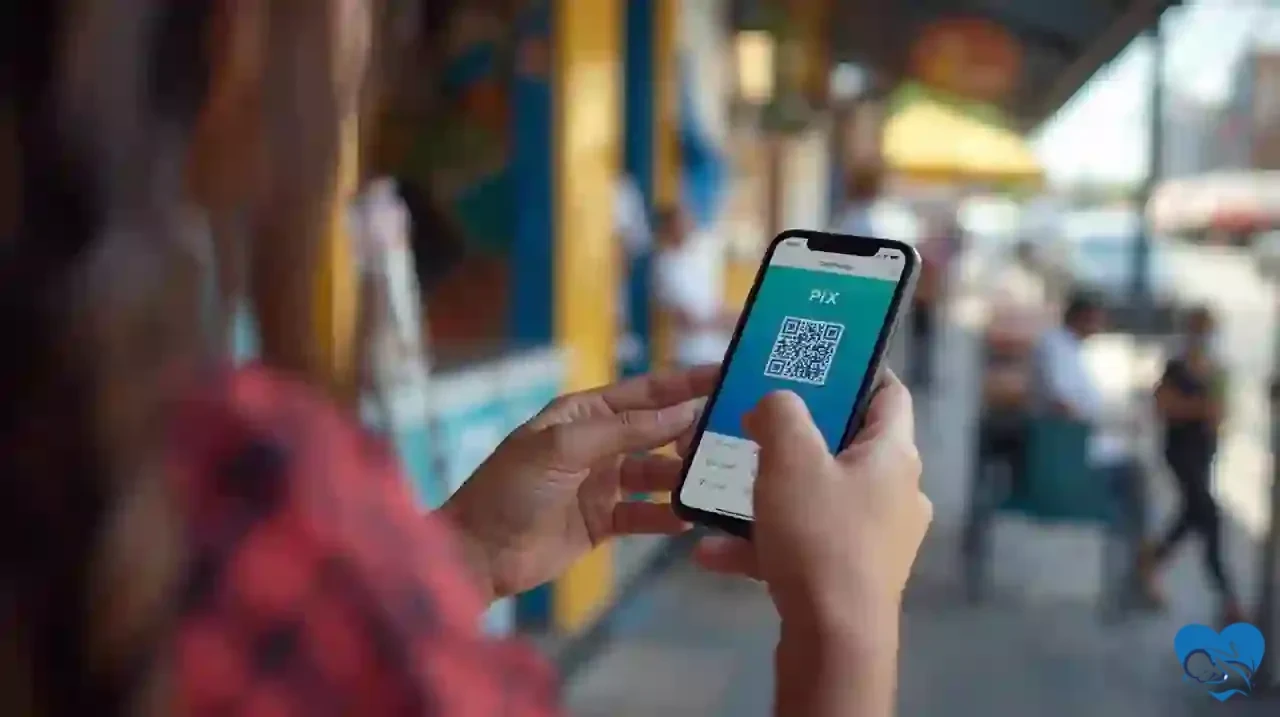

- PIX: Brazil’s star innovation – an instant payment system launched in 2020. With PIX, you can transfer money to others in seconds, 24/7, using simple “keys” (like your CPF, phone number, email, or random code). It’s free for individuals. You’ll definitely want to set up PIX keys in your banking app (most apps prompt you). With PIX, you can pay merchants, split bills with friends, or even pay some taxes instantly. By 2026, PIX is ubiquitous – even street vendors use PIX QR codes. It’s far more common than writing checks (few people use personal checks nowadays). As an expat, you’ll find PIX extremely convenient for paying your landlord, domestic help, or marketplace sellers.

- Boleto: A boleto is a payment slip with a barcode that you can use to pay bills or invoices. For example, utilities and internet bills often come as boletos. You can pay a boleto through your banking app by scanning the barcode or entering its numeric code, debiting your account. If you don’t have an account, you’d have to pay these in cash at a lottery house or bank branch – another reason an account is crucial.

- Debit vs Credit: Your bank card can function as a debit card (linked to your checking account balance). Getting a credit card as a foreigner can be trickier – digital banks might issue a low-limit credit card initially, but many expats start with just the debit function. Over time, as you use the account, you might get offers for a credit card. Credit in Brazil is subject to high interest rates, so many Brazilians use installment plans rather than carrying a balance on credit cards. If you do get a Brazilian credit card, note that any purchases in foreign currency will incur IOF tax (see tax section below) – many expats prefer to maintain a foreign credit card for international purchases and use the Brazilian account/card for local purchases.

- ATM Withdrawals: With your debit card, you can withdraw cash from ATMs. Major bank ATMs (Bradesco, Banco do Brasil, Itaú, etc.) accept the cards of their own and often other networks. Brazil also has independent ATMs like Banco24Horas (which work with a variety of banks). As an account holder, try to use your bank’s own ATMs for fee-free withdrawals. Using another bank’s ATM may incur a fee (usually a small amount like R$5-10). Digital banks often don’t own ATMs, but have agreements (e.g. Nubank clients use Banco24Horas ATMs a few times for free, then pay a fee). Plan accordingly. Cash use is decreasing but you’ll still need cash for some small vendors, local markets, or places that give a discount for cash.

- Bank Hours and Online Services: Bank branches in Brazil typically open from 10am to 4pm on weekdays. But with digital banking and widespread online services, you rarely need to visit. Use online banking or apps for almost everything. Customer service for digital banks is via chat in the app (Nubank is known for quick, helpful support). Traditional banks have phone and branch support – some have English-speaking staff at certain locations.

- Security: Brazilian banks use multiple layers of security. It’s common to have a 6-digit PIN for the card, a different internet banking password, and possibly a physical or app-based token code for confirming transactions. This can be cumbersome but is important. Never share your token codes or passwords. Scams exist (like fake calls asking for your info), so be vigilant. The banking apps themselves are secure – always download official apps and keep your phone’s OS updated.

- Internal Bank Transfers: Apart from PIX, you can also do traditional transfers: TED or DOC (these are older transfer systems within Brazil). PIX has largely replaced them for individuals because PIX is instant and free, whereas TED/DOC might have fees and cut-off times. But you might hear these terms, e.g. “Faz um TED para minha conta” (do a TED transfer to my account) – you can do it, but PIX is easier.

- Currency in Account: Regular personal accounts in Brazil are in BRL only. Unlike in some countries, you typically cannot hold a standard checking account in USD or EUR (some banks offer separate foreign currency investment accounts, and C6 or Inter digital banks have multi-currency sections). But your day-to-day account will be BRL denominated. When you bring dollars/euros into it, the bank will convert to BRL. If you plan to keep large sums in foreign currency, talk to your bank about authorized foreign currency accounts or use international platforms.

Now that we’ve established how to get and use a bank account, let’s move on to transferring money across borders – an area every expat deals with, whether bringing savings into Brazil or sending money back home.

Transferring Money To and From Brazil

Related reading: Finance & Taxation | Guide to Moving to Brazil | Cost of Living | Q&A

How much IOF applies? Short answer: it depends on the transaction category, but the guide’s working benchmarks are light inbound FX taxation and materially heavier outbound personal remittance taxation. Before any large transfer, confirm the live rate and legal classification with the executing institution.

Section summary

For most expats, the smartest comparison is not bank versus cash, but inbound versus outbound costs, documentation, and tax treatment. In practice, fintech remittance services often win on speed and total cost, while large outbound transfers require extra planning.

Moving money internationally can be one of the more complex (and costly) aspects of expat life. Brazil, while not as restrictive as some countries, still has regulations and taxes on foreign exchange that you need to navigate. In this section, we’ll discuss the best ways to send money to Brazil, how to send money out of Brazil, what costs to expect (exchange rates, fees, and taxes like IOF), and tips for getting the most out of currency exchange. We’ll also explain Brazil’s customs rules on carrying cash and how to safely exchange currency once you’re in the country.

Summary box — money transfers and FX costs

- Inbound transfers are usually easier and cheaper than outbound transfers.

- The real cost is rarely just one fee: compare FX spread, service fee, IOF, settlement speed, and documentation requests together.

- Keep proof of origin and purpose for larger transfers; documentation friction usually appears when the amount gets meaningful.

- For day-to-day life, the cheapest workflow is often a BRL account plus PIX plus a specialist remittance service when you actually need cross-border movement.

Sending Money to Brazil (Inbound Transfers)

Related reading: Finance & Taxation | Remote Work in Brazil | Employment in Brazil

{kind=link}

| Topic | Sending money to Brazil (inbound) | Sending money from Brazil (outbound) |

|---|---|---|

|

Typical best route |

Fintech remittance services or a clean bank wire for larger amounts. |

Bank wire, remittance platform, or specialist FX workflow depending on size and purpose. |

|

Planning benchmark |

Usually simpler, with lighter tax drag and faster settlement. |

Usually more paperwork-sensitive, with heavier tax drag on common personal remittances. |

|

What matters most |

FX spread, receiving-bank handling, and proof of source for large transfers. |

IOF category, purpose code, origin-of-funds support, and timing. |

|

Speed |

Often minutes to a few business days depending on provider and currency pair. |

Often a few business days, with more room for compliance checks. |

|

Best practice |

Bring money in through documented, transparent channels and keep transfer receipts. |

Plan large repatriations early and match the transfer purpose to the correct legal category. |

Options to send money into Brazil:

- International Bank Wire (SWIFT transfer): You can wire money from your foreign bank to your Brazilian bank. You’ll need your Brazilian bank’s SWIFT/BIC code and your account details. Wires are secure but can be slow (2-5 days) and expensive – foreign banks charge fees, and Brazilian banks often charge to receive (plus they may give a less-than-market exchange rate). Expect intermediary fees as well. For large amounts, this is a straightforward method, but inquire about fees on both ends. Brazilian banks typically charge a fixed fee (e.g. R$100) to process an incoming wire and will automatically convert the funds to BRL upon arrival at a rate slightly below market.

- Online Remittance Services (Fintechs): This is often the cheapest, fastest method. Services like Wise (formerly TransferWise), Remessa Online (a Brazilian platform), Western Union, MoneyGram, Xoom, etc., allow you to send money by paying in from your foreign account/card, and the service deposits reais to your Brazilian account. These services usually give a much better exchange rate (close to the interbank rate) and charge a transparent fee. For example, Wise might charge ~0.4-1.5% depending on currency, far better than the 5-8% total cost of using a foreign bank/card. Remessa Online is Brazil-based and popular for bringing money in; it often has tiered fees (e.g. a small percentage). Western Union and MoneyGram allow cash pickup, but also can deposit to bank accounts – their rates vary, sometimes competitive for small amounts, not for large.

- Cryptocurrency or Alternate: Some expats have used crypto to move money (buy crypto abroad, sell in Brazil for BRL). While some have found workarounds this way, we don’t recommend this for most users due to regulatory uncertainties and potential for fraud or big price swings. It also doesn’t bypass tax obligations – converting crypto to BRL in Brazil might trigger the same reporting as a cash transfer. Use regulated channels when possible.

- Bringing Cash and Exchanging: We’ll cover carrying cash under currency exchange, but briefly: you could physically bring foreign currency and exchange it in Brazil. This avoids transfer fees, but you’d have to deal with the safety of carrying cash and finding a good exchange bureau.

What about receiving salary from abroad? If you’re a remote worker paid by a foreign company, you might use services like PayPal or Payoneer, or have your company wire money. PayPal is widely used but their currency conversion rates are usually poor and fees high. A better route can be Payoneer or Wise’s multi-currency account (you get local account details in USD/EUR etc., your employer pays there, then you transfer to your Brazil account at good rates). Also, some Brazilian digital banks (e.g. Banco Inter) have features for receiving international transfers cheaply – Inter partners with Wise for instance. Investigate those if you have frequent foreign income.

Costs and Taxes on incoming funds: When you send money to Brazil, two main costs apply: service fees/exchange spread, and IOF tax.

- Service fees/exchange: If you use a service like Wise, the fee is built-in. If you do a wire, the sender’s bank and intermediary banks will levy fees (maybe $20-$40 in total), and your Brazilian bank may convert at a less favorable rate (hidden cost).

- IOF (Imposto sobre Operações Financeiras) on exchange: For incoming transfers, Brazilian law charges IOF on the currency exchange operation when converting foreign currency to BRL. The IOF rate for most incoming remittances is currently 38%. (This is after a 2025 change that standardized many rates; previously it was 0.38% for most cases and would have gone to 0% by 2028, but plans changed.) The 0.38% IOF is a minor tax – for example, sending $10,000 worth of currency would incur about $38 of IOF when converted to reais. Some specific types of transfers can be exempt or different, but general personal remittances will see 0.38%. The IOF is usually deducted by the receiving bank automatically during conversion.

Documentation: If you’re transferring large sums (especially above the equivalent of R$100,000), Brazilian banks might request you declare the reason (e.g. “own savings transfer”, “family support”, “investment in property”) and possibly evidence (like a contract if it’s to buy a house, etc.). For routine smaller amounts, you won’t typically be asked for documents, but the transfer will still be tagged with a purpose code by the bank. Make sure to truthfully classify the transfer (when you fill the form abroad, select the correct reason if available, e.g. “family maintenance” or “personal savings”). Brazilian exchange regulations require transparency but are not there to prevent you from bringing money – they just want to ensure it’s not illicit. There is no limit to how much you can bring into Brazil via bank transfers, as long as you can show it’s legitimate if asked.

Speed: Services like Wise can deliver BRL to your account in minutes or hours for major currency pairs, or a day or two for more exotic routes. Bank SWIFT transfers typically take 2 business days to land in Brazil after leaving the origin bank (assuming no hiccups).

Example – Using Wise: John needs to send £5,000 from the UK to his Brazilian account. He goes on Wise, which quotes him an exchange rate only ~1% below the mid-market and a fee of about 0.7%. He pays Wise via a debit card or local bank transfer in the UK. Within one day, Wise deposits Brazilian Reais in John’s account, with an IOF of 0.38% automatically applied. John ends up with the money quickly and with minimal loss to fees. If he had done an international wire from his UK bank, he might have paid a fixed £20 fee plus gotten 3-4% worse exchange rate – costing perhaps £150 more than Wise’s method.

Recommendation: For most expats, online remittance services (fintechs) are the way to go for sending money to Brazil. Use bank wires only for very large amounts where you prefer dealing bank-to-bank or if you have no fintech option from your origin country.

Sending Money from Brazil (Outbound Transfers)

Related reading: Finance & Taxation | Permanent Residency | Guide to Moving to Brazil

{kind=link}

Sooner or later, you may need to send money out of Brazil – for example, to support family back home, to pay an overseas mortgage, or to move savings when you leave. Outbound transfers have historically been more cumbersome due to Brazilian regulations, but it’s absolutely legal to send your money out as long as taxes are paid and reasons documented. Here’s how:

Options to send money out of Brazil:

- International Wire from your Brazilian bank: This is the traditional method. You instruct your Brazilian bank to wire funds to a foreign account. Many banks require you to go in person to authorize an international transfer (or, if allowed, through their internet banking with a special token). You’ll fill out a form indicating the destination, amount, currency, and purpose (there’s a list of purpose codes, e.g. family maintenance, loan payment, asset transfer, etc.). The bank will perform the currency conversion from BRL to, say, USD or EUR, then send the wire. Fees on the Brazilian side can be a few hundred reais. The exchange rate may have a spread. This method is fine for large amounts or regular transfers, but note the tax implications below.

- Remittance Services (Wise, etc.): Until recently, sending money out of Brazil via services like Wise was limited. Wise does support BRL transfers out, but often requires you to have a Brazilian boleto or bank debit (Wise will give you instructions to send a TED to their local account, then they send out foreign currency). Brazilian regulations have made it a bit tricky, but as of 2025, with more open currency rules, such services might become more streamlined. Remessa Online (Brazil-based) allows sending money abroad too – you register, prove your ID and tax compliance (they may ask for your tax ID and maybe proof taxes paid on the money), then you can send out. Expect to provide documentation especially for larger values going out (to show the origin of funds was legal and taxed).

- Bitcoin/Crypto route: Some individuals have circumvented high fees by buying cryptocurrency in Brazil (often via an exchange), then selling it abroad. This can technically move money, but it carries risk and potential tax reporting complexities. It’s beyond the scope of this guide for detailed steps, and not recommended unless you’re well-versed and willing to accept volatility.

Costs and IOF on outbound:

Here’s the crucial part: Brazil imposes IOF tax on many outbound money transfers, and it’s significantly higher than on inbound. In May 2025, the government increased the IOF on most outbound foreign exchange transactions to 3.5%. This is a big jump from the previous 0.38% and was done to raise revenue, reversing a plan to reduce IOF.

What does this mean? If you send money from your Brazilian account abroad (for example, converting R$100,000 to USD and wiring out), you could incur a 3.5% IOF tax on the BRL amount. That’s R$3,500 on R$100k – a significant cost. However, there are exceptions:

- If the transfer is categorized as investment abroad (i.e. sending money to buy stocks or real estate abroad in your name, etc.), the IOF is 1%. The definition of “investment purposes” as of the decree is a bit technical, but generally personal remittances to yourself can often be structured as “investment” if you declare that (banks have codes for that).

- Certain transactions remain 0% IOF (for example, foreign investors pulling out capital they invested in Brazil’s markets remained at 0%, and paying dividends or interest abroad is 0%), but those likely don’t apply to typical expat personal transfers.

- The 5% IOF specifically hits things like: transferring money to your own account abroad for general use, sending money to family abroad, buying foreign currency in cash, or loading prepaid cards. So it’s broad.

So, if you’re planning to repatriate a large sum (like proceeds from selling your Brazilian apartment, or accumulated salary savings), be prepared for that IOF cost. It might be worthwhile to consult with your bank or a specialized exchange broker to see if your transfer can be classified under the lower 1.1% category (e.g. maybe framing it as an investment or loan to yourself abroad – something within legal bounds).

Other fees: Your Brazilian bank will likely charge a fixed fee (maybe R$150-300) for the international wire. And the exchange rate they give might include a 1-2% spread. If using Remessa Online or Wise for outbound, their fees+spread might be around 2% or less, which might offset some of the IOF – but note, IOF is unavoidable as it’s a tax. Wise might not explicitly show IOF but it’s embedded when they do local conversion.

Documentation for outbound: Definitely, if you send higher amounts, the bank will want to know the reason. Common legitimate reasons: - Salary repatriation (e.g. sending part of your earnings to support someone abroad). - Family support. - Savings transfer. - Property purchase abroad or investment. - Loan repayment (if you’re sending money to pay a loan abroad). Each will have a code. If the money you’re sending was earned in Brazil, ensure you’ve paid any due Brazilian income taxes on it before sending. If it’s money you originally brought in (capital that you now want to take back out), it’s good to have records of the initial inbound transfer, so you can show it’s principal being returned (though legally, if you became a resident, that money turned into local currency and any gains are taxed, but the principal can go out freely).

Brazil doesn’t have foreign exchange controls in the sense of preventing you from taking money out, but they do enforce the IOF and reporting. Always channel transfers through the formal banking system or authorized operators so that you have a documented trail. Attempting to smuggle cash or use under-the-table exchanges is illegal and risky.

Time frame: Outbound bank wires from Brazil can also take 2–3 business days. You might find Brazilian banks are sometimes slower with outbound than inbound, due to compliance checks.

Using PIX International (forthcoming): Brazil has been working on connecting PIX internationally (PIX is domestic currently, but there’s discussion of linking it with other instant payment systems globally). By 2026, there’s talk but not yet reality for most corridors. If/when that happens, sending money abroad might become as easy as PIX, but for now, we use the methods above.

Example – Outbound scenario: Maria, after working in Brazil for a few years, decides to move back to Europe. She wants to send the equivalent of €30,000 from her Brazilian savings to her German bank. She goes to her Banco do Brasil branch and requests a wire, marking it as personal savings transfer. The bank converts her R$ (let’s say roughly R$160,000 for €30k at the time) to euros. They apply 3.5% IOF (R$5,600) – ouch – and charge a R$200 fee. Maria ensures she has paid income tax on all her Brazilian earnings and keeps the receipts, just in case. Within 3 days, the euros arrive in her German account. In hindsight, Maria realizes if she had gradually moved money via Wise earlier, each smaller transfer might’ve also incurred IOF (which is automatically included) but maybe less noticeable – however, the 3.5% tax is the law regardless of method for a personal outbound transfer. She includes the detail of this transfer in her Brazilian final tax declaration (since leaving) and in any required foreign asset reporting in Germany.

Bottom line: Plan your outbound transfers carefully. If you know you’ll leave Brazil with significant funds, consider timing (the IOF rate is high now, but Brazil has floated plans to reduce IOF for international transfers to 0 by 2029 in line with OECD agreements – though these were put on hold and even reversed in 2025). Keep an eye on legal changes. It might also be worth consulting a specialized foreign exchange broker in Brazil who might get you a slightly better net deal (some brokers might absorb part of the IOF or have creative solutions if it’s a truly large amount, though they must still collect the tax legally).

Currency Exchange in Brazil (Cash and Conversion Tips)

Related reading: Cost of Living | Finance & Taxation | Regulation Changes

{kind=link}

If you have foreign cash or need to convert money once in Brazil, here’s what to know:

- Exchange Bureaus (Casas de Câmbio): These are licensed money changers. You’ll find them in airports, major shopping malls, and city centers. They will exchange major currencies (USD, EUR, etc.) for reais. Rates can vary widely. Airport exchanges notoriously give poor rates (convenience fee). In the city, compare a couple of bureaus if you can. Always present your passport when exchanging – by law they will log your ID for any amount (especially for amounts at or above US$3k, they must register the transaction to your CPF as well). The posted rate usually includes their fee. Some bureaus might negotiate if you are exchanging a larger amount – no harm in asking for a slightly better rate if changing thousands of dollars/euros.

- Banks: Some bank branches (especially Banco do Brasil or Bradesco in tourist areas) can exchange currency for you if you have an account, possibly at decent rates, but many retail branches don’t handle cash exchange for walk-ins nowadays, steering you to ATMs or exchange bureaus.

- ATM Withdrawals with Foreign Card: If you have an overseas bank card, you can simply withdraw reais from an ATM in Brazil. This is often a convenient way to get local cash, but watch out for fees. Your home bank may charge a withdrawal fee and 1–3% foreign transaction fee, and the Brazilian ATM’s bank might charge a usage fee. Also, your home bank’s exchange rate might have a spread. Still, for moderate amounts, it’s an easy solution. Prefer major bank ATMs (Bradesco, Banco do Brasil, Santander) or the red “Banco24Horas” multi-bank ATMs. Note: Many Brazilian ATMs have a per-withdrawal limit (sometimes R$500 or R$1,000 for foreign cards), so you might have to withdraw multiple times (incurring fees each time).

- Using Credit Cards: Using a foreign credit card for purchases in Brazil will get you cashless convenience, but it comes with typically a 5-7% total cost (bank fee + worse exchange + Brazilian IOF of 5-6%). Brazilian merchants charge your card in reais; your card network converts it to your currency. Brazil adds a hefty IOF tax of currently 3.5% on foreign currency credit card transactions (recent changes have reduced it from the long-standing 6.38% to 3.5% for most cross-border purchases, though confirm if your card issuer reflects the updated rate). That IOF is on top of any fees your card imposes. So, while credit cards are fine for convenience or emergencies, they’re not the best for large expenses. However, if you have a no-foreign-fee card and can pay it off fully, using it for day-to-day spending might give you a decent exchange rate (Visa/Mastercard wholesale rate) plus just the IOF. Many expats use a mix: local debit/Pix for most things, and a foreign credit card sparingly or for online bookings.

- Carrying Cash into Brazil: If you plan to bring physical cash (in foreign currency) when traveling to Brazil, know the customs regulation: you can bring in up to USD $10,000 (or equivalent in any currency) per person in cash without declaring. If you carry more than $10k, you must declare it via the online “Traveler’s Electronic Declaration of Goods (e-DBV)” before you arrive, and present the declaration at customs. There is no tax on bringing cash, it’s just a reporting requirement. The limit was updated in 2022 to align with international standards (it used to be a fixed R$ amount, now it’s USD 10k or equivalent). If you fail to declare amounts over that, they might seize it or fine you. So if a couple is traveling, they could theoretically bring $9k each undeclared (total $18k). But carrying large sums is risky. Once in Brazil, you’d then have to exchange that cash – doing so safely at a bank or bureau (large cash exchanges might actually fetch slightly better rates if you shop around, but be very cautious carrying cash around).

Exchange Rate Considerations: Keep an eye on the “dólar comercial” vs “dólar turismo” rates. In Brazil, the commercial rate is the interbank rate, whereas turismo (tourism) rate is what individuals get at exchange shops – typically 3-5% worse than commercial. If the mid-market is R$5.00 per USD, a bureau might quote R$4.85 (if they charge a high commission) or R$4.95 (better) for buying dollars. For euros, similar concept. Timing currency exchange is always a bit of speculation; the Real can be volatile, so some expats convert a bit at a time rather than all at once, to average out the rates.

IOF on currency exchange in cash: When you go to an exchange bureau and give them $100 to get reais, there is an IOF tax of 0.38% usually embedded in that too – but typically the bureau handles it in the rate or price. If you use your Brazilian account to buy foreign currency (like getting dollars for a trip), you pay 1.1% IOF on that currency purchase in cash (this was also raised to 3.5% in 2025, but the decree specifically mentions purchase of foreign currency in cash at 3.5% – which seems contradictory to earlier rules of 1.1%; it appears the new rule set it uniformly 3.5% for buying cash too). That means, ironically, exchanging money in Brazil has become heavier taxed if you’re doing it through official channels. Many travelers have felt this with credit cards historically (6.38% IOF), now somewhat better if it’s indeed 3.5%. The tax policy is in flux, but as an expat, you mostly encounter IOF automatically when doing these transactions, so just be aware it exists.

Don’t Use the “Parallel Market”: In some countries, a black market for currency thrives (e.g. Argentina). In Brazil, a parallel market exists but is not as prevalent; stick to legal exchanges. It’s not worth the risk of counterfeit notes or getting caught in a sting. The official channels are reliable, and since 2022, rules have modernized to make transactions easier (like raising the cash carry limit and allowing non-resident accounts).

Best Practices for Managing Exchange and Transfers

Related reading: Finance & Taxation | Local Bureaucracy | Q&A

To wrap up the money transfer and exchange section, here are some best practice tips:

- Plan large transfers in advance: If you know you need to move a large amount, consult both your home bank and a fintech to compare costs. Sometimes splitting into multiple smaller transfers over time can save IOF (though in Brazil’s case IOF is percentage, so splitting doesn’t change that tax, but it could allow you to ride the exchange rate if it improves).

- Keep proof of all transfers: Save receipts or confirmation screenshots of every international transfer. They show the origin of funds which can be useful for tax or for remitting out later (especially if you ever need to prove that money you’re taking out was initially brought in legitimately).

- Use local currency (BRL) for local expenses: Exchange what you need to reais (or better, use your Brazilian bank/Pix) for spending in Brazil. Avoid paying in your home currency if a merchant offers “dynamic currency conversion” on your card – always pay in BRL, the rates will be better via your bank than the merchant’s conversion.

- Monitor exchange rates: The BRL can swing with political or economic news. If you’re not in a rush, you might exchange in batches when the rate is favorable (e.g. Real strengthens or weakens depending on what side you’re on – as an expat bringing money in, you like a stronger foreign currency vs Real; when taking money out, you prefer a stronger Real).

- Mind the Regulations: Stay within legal limits for carrying cash and always declare when required. Also ensure you comply with any foreign account reporting at home (e.g. Americans must file FBAR if total foreign accounts > $10k).

- Consult an Expert for Complex Cases: If you’re transferring proceeds from a property sale or very large sums, consider using a specialized currency broker or consulting a financial advisor. There might be specific rules (for instance, if you brought money to Brazil to buy property and are now selling property and repatriating, you can repatriate the original capital without Brazilian tax, but any capital gain is taxed; you’ll need to sort that out).

- Be aware of scams: Only use known, trusted services. If someone offers a too-good rate informally, be cautious. Brazil has strict AML (anti-money laundering) controls, so any attempt to bypass the system could land you in legal trouble.

Having tackled banking and money movement, it’s time to address the other side of financial life in Brazil: taxation. The next sections will delve into Brazil’s tax system for expats – what income is taxed, how to file, and your obligations as a foreign resident (including some often overlooked requirements).

Taxes in Brazil for Expats

Related reading: Finance & Taxation | Work & Business | Remote Work in Brazil | Opening a Business in Brazil

Do expats pay tax on foreign income in Brazil? Short answer: once you are a Brazilian tax resident, Brazil generally taxes worldwide income, although foreign tax credits, treaty rules, and recognized reciprocity can reduce double taxation.

Section summary

Three questions drive most expat tax outcomes in Brazil: when you became a resident, whether the income is Brazilian or foreign-source, and whether treaty or credit relief is available. Once you organize those three points, the rest of the compliance picture becomes much easier.

Finances aren’t just about banking – managing your tax obligations is equally important. Brazil’s tax system can be complex, especially for foreigners dealing with income from multiple countries. This section serves as an expat’s roadmap to Brazilian taxes: we’ll explain who is considered a tax resident, how your income (Brazilian and foreign) will be taxed, the tax rates and brackets, how to file your annual Imposto de Renda (income tax return), what credits or deductions you might use, and how to avoid being taxed twice on the same income. We’ll also touch on other taxes you might encounter (like on investments or services) and the procedures when you arrive or leave Brazil, such as notifying the tax authorities.

Tax Residency: Who Pays Taxes in Brazil?

Related reading: Visa Requirements | Permanent Residency | Moving to Brazil with Family

{kind=link}

| Situation | Likely status | Practical consequence |

|---|---|---|

|

You spend more than 183 days in Brazil within a 12-month period. |

Usually resident |

Worldwide income usually enters the Brazilian tax analysis. |

|

You enter under a scenario that makes residency start from arrival. |

Usually resident from entry |

Do not wait for the 183-day count before reviewing tax obligations. |

|

You stay in Brazil short-term and remain below the residency trigger. |

Usually non-resident |

Brazil generally focuses only on Brazilian-source income. |

|

You leave Brazil but do not formalize final departure. |

Residency may linger |

You can create avoidable filing, penalty, and status problems. |

When do you become a tax resident? Short answer: in many expat cases, residency begins after more than 183 days in Brazil within a 12-month period, but some permanent or work-linked entry situations can make the tax clock start from the day you enter Brazil.

| Topic | Resident in Brazil | Non-resident in Brazil |

|---|---|---|

|

Scope of taxation |

Generally taxed on worldwide income. |

Generally taxed only on Brazilian-source income. |

|

Annual return |

Usually files an annual Brazilian income tax return if thresholds are met. |

Usually relies on withholding at source and does not file a normal resident return. |

|

Foreign income |

Usually reportable and potentially taxable in Brazil. |

Usually outside Brazil’s tax net. |

|

Brazilian-source income |

Included in the resident tax calculation. |

Usually taxed by final withholding rules. |

|

Departure handling |

Must formally end residency to stop resident treatment cleanly. |

Already outside the resident system, but still subject to source-based rules. |

At-a-glance rule

For most expats, Brazilian tax residency is triggered either by spending more than 183 days in Brazil within a 12-month period or by entering under a scenario that causes residency to start from arrival. Always align the tax analysis with your exact immigration pathway and date of entry.

Tax residency in Brazil determines how you are taxed. It’s possible to be living in Brazil but not be a tax resident (for a short time), or conversely, be outside Brazil but still considered a resident until you officially exit the system. Here are the rules:

- Becoming a Tax Resident: Generally, you become a tax resident in Brazil if you reside in Brazil for more than 183 days (about 6 months) within any 12-month period. The days need not be consecutive; they count cumulatively. The count typically starts from your date of entry with a visa that allows long-term stay (not a short tourist visit).

- If you come on a permanent visa or certain work visas, you are a tax resident from the day you enter Brazil on that visa.

- If you come on a temporary visa (like a student or job-seeking visa) that is longer-term, you become resident after 183 days.

- Special case: Digital nomad visa holders and the like – there is no special tax exemption currently; if you physically stay past 183 days, you’re a resident for tax purposes (even if your income is foreign).

- Non-Resident status: If you stay in Brazil less than 183 days in a 12-month period and do not hold a residence visa, you remain a non-resident for tax purposes. As a non-resident, you’re only taxed in Brazil on your Brazilian-source income (more on that below), typically via withholding at source. Non-residents do not file annual Brazilian tax returns for those non-resident years.

- When residency starts and ends: For someone arriving without a permanent visa, your 183-day clock resets every time 12 months passes from the date of first entry. For example, if you first arrived Jan 1 and stayed 4 months, left, came back later – you track within that year.

- If you become a resident and then leave Brazil, you remain a tax resident until you either (a) stay out of Brazil for more than 12 months or (b) file a Final Departure Tax Declaration to notify the government you ceased residency (more on that in the departure section). So without formal exit, an expat who leaves in July might technically still be resident for the rest of that calendar year (and taxed on worldwide income).

- Example: Alice arrives in Brazil on a work contract in March 2026. By end of August 2026, she’s been in Brazil for over 183 days, so she became tax resident sometime in September 2026. She will file a tax return for 2026 reporting worldwide income from the date she became resident (there are special partial-year rules). Conversely, Bob comes for an extended 5-month trip and leaves – he stayed 150 days, never crossing 183, so he stayed a non-resident and owes taxes only on any Brazilian-source earnings (if any) during those months, with no annual return needed if none.

Implications of being a Tax Resident vs Non-Resident:

- Tax

Residents are

taxed on their worldwide income by Brazil. That means if you are a resident, any

salary,

self-employment income, investment earnings, rental income etc., from any country is

subject to

Brazilian tax (Brazil might give credits or treaty benefits to avoid double taxation, but you must

declare it). You

will likely need to file an annual tax return (Declaração de Imposto de

Renda) each

year by April. - Non-Residents are taxed only on Brazilian-sourced

income, and

typically at a flat withholding rate with no deductions. If a non-resident has Brazilian income (like

consulting

fees, rental of a property in Brazil, etc.), the payer withholds a flat tax (usually 25% for many types

of income if

you’re from a “tax haven” or 15% otherwise). Non-residents do not get to file an

annual return to

adjust anything – the withholding is final. And non-residents don’t pay tax on foreign

income to Brazil

at all.

In short, once you pass the residency threshold, Brazil claims a piece of all your income globally (similar to US/UK/Canada, etc., though with some relief measures).

Documentation on arrival: Unlike some countries, Brazil doesn’t require you to register with the tax authority upon becoming a resident – your CPF is the tax ID and you likely already have it. However, if you start working in Brazil, your employer will register you for payroll taxes. If you have no Brazilian employer (e.g. digital nomad living off foreign income), it’s on you to start complying (more on how to pay tax on foreign income in the next section).

(Important: “Residence for tax purposes” is separate from immigration residency status. It is possible to be a legal resident (with visa) but spend little time and thus not be considered a tax resident for a given year, though usually if you have a permanent visa and stay less than 183 days, you might technically still be considered resident from day one under the rules, so careful. Always check the exact criteria for your situation – e.g. permanent visa triggers residency immediately.)

Summary box — tax residency before tax rates

- The biggest threshold is not the tax rate; it is the moment you become a Brazilian tax resident.

- Once you are resident, Brazil can pull worldwide income into the picture, which changes reporting and planning immediately.

- Track your days, your visa or residence status, and your foreign income from day one instead of trying to reconstruct the year later.

- If you expect to leave Brazil again, plan the eventual departure filings before the first filing season arrives.

Brazil’s Income Tax System: Rates and What’s Taxed

Related reading: Finance & Taxation | Work Permits | Employment in Brazil

Brazil has a progressive income tax system for individuals, with rates from 0% up to 27.5%. While 27.5% sounds low compared to some countries, remember Brazil’s thresholds for reaching that top rate are relatively low in terms of income. Also, unlike some countries, Brazil does not have significant itemized deductions for individuals (limited deductions exist for dependents, some education and medical expenses, etc., but not things like mortgage interest).

Taxable income includes: salaries, self-employment income, pensions, investment income (interest, certain capital gains), rental income, and foreign income (if you’re tax resident). Some specific types of income have separate rules (e.g. Brazil doesn’t tax dividends from Brazilian companies at the individual level currently, and certain savings interest is exempt).

Personal Income Tax Rates (Monthly Table): Brazil uses a monthly tax withholding table for salaried income, and the same brackets apply when calculating the annual tax due. As of 2024, the monthly income tax brackets are:

- Income up to R$2,259.20 per month – Exempt (0% tax).

- Income from R$2,259.21 to R$2,826.65 – 5% tax rate (minus a fixed deduction of R$169.44).

- R$2,826.66 to R$3,751.05 – 15% rate (minus R$381.44).

- R$3,751.06 to R$4,664.68 – 5% rate (minus R$662.77).

- Above R$4,664.68 – 5% rate (minus R$896.00).

Those “minus R$X” amounts are used in monthly payroll for easing calculation. Effectively, if you earn above ~R$4,664 (about USD $900) per month, the portion above is taxed at 27.5%. Any income below ~R$2,259/month is not taxed at all. These numbers get adjusted occasionally for inflation, but until recently they were quite low, causing even modest earners to pay some tax. (There was talk of raising the exemption to R$5,000/month in 2023, but instead it was slightly adjusted by 2024 to the numbers above.)

If you think annually: R$4,664/month is about R$55,975/year (roughly USD $10,000/year). So Brazil’s top bracket starts at a low level of income by developed country standards (meaning many middle-class professionals already hit 27.5%). On the flip side, 27.5% is the ceiling – high earners don’t face 40%+ as in some other countries. There are no higher rates for ultra-high incomes (though proposals have been floated for new brackets).

Non-Residents Flat Tax: As mentioned, if you are a non-resident, any Brazil-source income is typically taxed at a flat 15% (or 25% if you reside in a “low-tax jurisdiction” or for certain types like royalties). For example, a non-resident consultant paid by a Brazilian client would have 15% withheld; a non-resident receiving Brazil dividends (currently exempt, as dividends aren’t taxed at distribution) would pay 0%; a non-resident earning rental on a property in Brazil pays 15% withheld at source.

What counts as Brazilian-source income? Generally, if the payer is in Brazil or the income arises from assets in Brazil: - Salary paid by a Brazilian employer = Brazilian source. - Self-employment services rendered in Brazil to a Brazilian client = Brazilian source. - Rent from property located in Brazil = Brazilian source. - Brazilian bank account interest = Brazilian source. - Foreign company paying you while you live in Brazil? That’s considered foreign source (since the payer is outside Brazil) – but if you are resident, you still must pay Brazilian tax on it (because worldwide income is taxed).

Foreign-source income for residents: If you’re tax resident and earn income from abroad (like remote work salary from a foreign company, foreign investment interest, etc.), Brazil expects you to pay tax on it monthly via a system called Carnê-Leão (literally “lion booklet”, referencing the tax authority’s symbol being a lion). Carnê-Leão is a monthly tax payment (like estimated tax) you calculate on untaxed income you received that month. For example, if you got US$2000 from abroad in a month as a freelancer, you’d convert to BRL using the official rate and apply the progressive table to find how much tax that income incurs, then pay it by the end of the next month to Receita Federal. The reason is to put foreign income on par with local salary that would’ve had withholding.

However, recent developments: In 2024, Brazil moved to simplify taxation of foreign income by making it annual in some cases (there was a law/bill in 2023 aiming to tax foreign earnings and investments on an annual basis at 0%, 15%, 22.5% depending on amount). This suggests that smaller foreign earnings (up to R$6,000/year) might be exempt, and above that taxed at certain rates. This was part of a tax reform bill (PL 4173/2023) targeting offshore investment income. If passed, it could mean that individuals would report foreign passive income (interest, dividends, etc.) in the annual return with these brackets rather than doing monthly carnê-leão. But for earned income (like salary), carnê-leão is still in place as of 2025. Always double-check current rules – as an expat, you may want an accountant to assist with monthly obligations if you have significant foreign income to declare.

Deductions and Credits: Brazil’s tax system allows a few personal deductions: - A fixed deduction per dependent (including children, or perhaps a non-working spouse if officially a dependent) – around R$2,275 per dependent annually (value as of mid-2020s; check current). - Education expenses for you/dependents up to a low cap (~R$3,700 per person annually). - Medical expenses – you can deduct qualifying medical and dental expenses in full (no cap) if you have receipts, one of the more generous aspects. - Contributions to Brazilian private pension plans (PGBL) up to 12% of your income. - The simplified deduction: Alternatively to itemizing, individuals can choose a standard deduction equal to 20% of income (capped at R$16,754 for the year). Many expats opt for simplified unless they have large medical expenses, because the caps on other things are low.

All these come into play when you do the annual return. If you are just earning salary in Brazil, your employer withholds tax each month and you file in April to reconcile (maybe you get a refund if you had deductible expenses or too much withheld, or you owe more if you had extra untaxed income).